Most explanations of algo trading either drown you in jargon or sell you a dream. Neither helps when you actually want to know: what happens between "I have a trading idea" and "an order hits my broker"?

This guide walks through that full pipeline the way it actually works for Indian retail traders. No HFT fantasy, no guaranteed-profit talk — just the real workflow, the checks at each stage, and where things tend to break.

What algo trading really means for retail

Algo trading is just executing a set of pre-defined rules automatically. The "algo" is your logic: an entry condition, an exit condition, a stop loss, a position size, and the universe of instruments you trade.

You are not competing with co-located institutional servers on microseconds. For a retail trader in India, the value is different and more practical:

- Rules run the same way every time, so emotion and hesitation are removed.

- The system can watch many symbols at once without you staring at screens.

- Every trade is logged, so you can audit what happened instead of guessing.

That last point matters more than speed. Discipline and record-keeping are where most retail edges actually come from. If you want the broader picture, the algo trading in India overview covers how the pieces fit together.

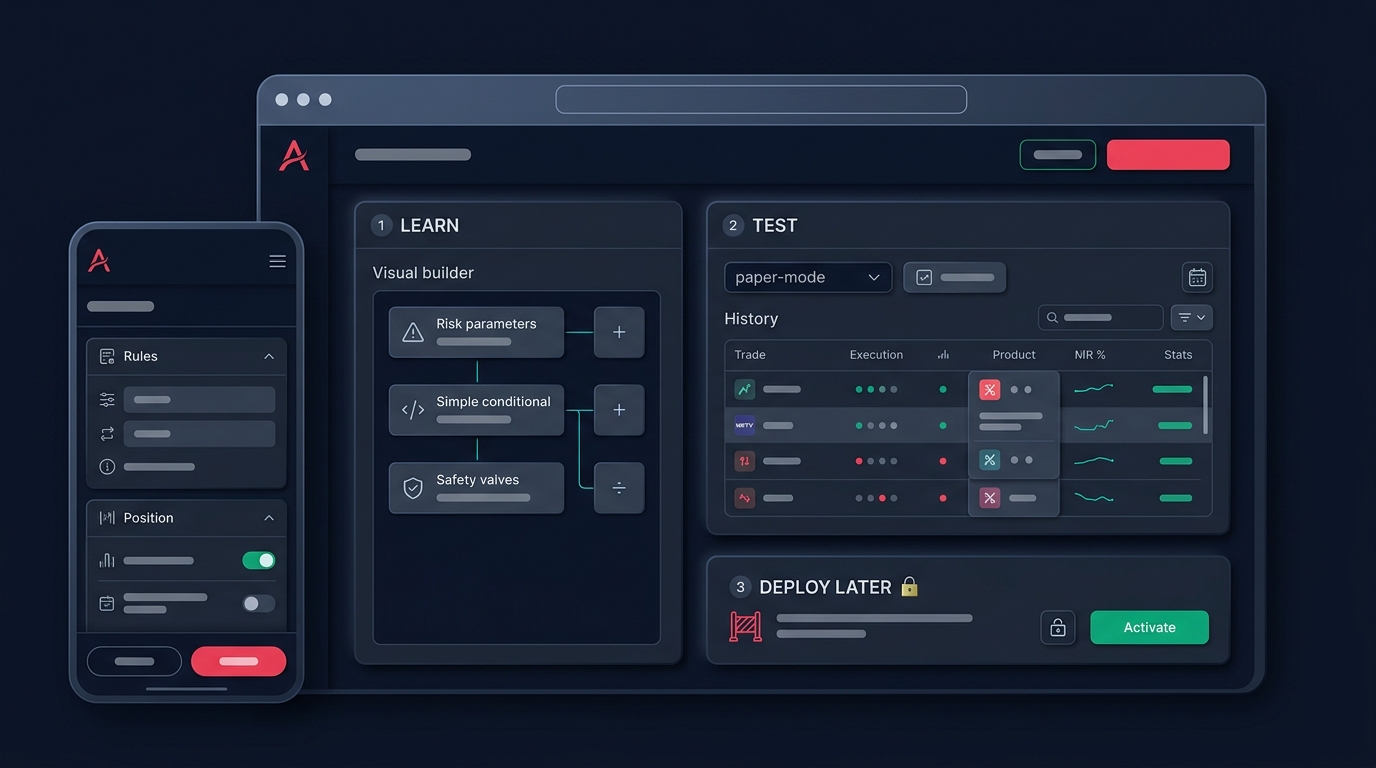

The workflow: rules to backtest to paper to live

The honest path has four stages, and skipping any of them is where accounts get hurt. Treat it as a funnel — each stage filters out ideas that look good but don't survive contact with reality.

Step 1: Turn an idea into exact rules

A trading idea in your head — "buy Bank Nifty when it breaks the morning high" — is not yet a strategy. A computer cannot act on "breakout" until you define it precisely.

What is the morning high — the first 15-minute candle, or the first hour? Break by how much — one point, or a 0.1% buffer to avoid noise? What is the stop, the target, and the maximum quantity? What happens if there is a gap-up open?

This is the step most traders rush. A no-code strategy builder or a chat-style wizard helps here by forcing you to fill in the missing fields: entry, exit, risk, sizing, and instrument universe. If you cannot state the rule in one unambiguous sentence, it is not ready to test.

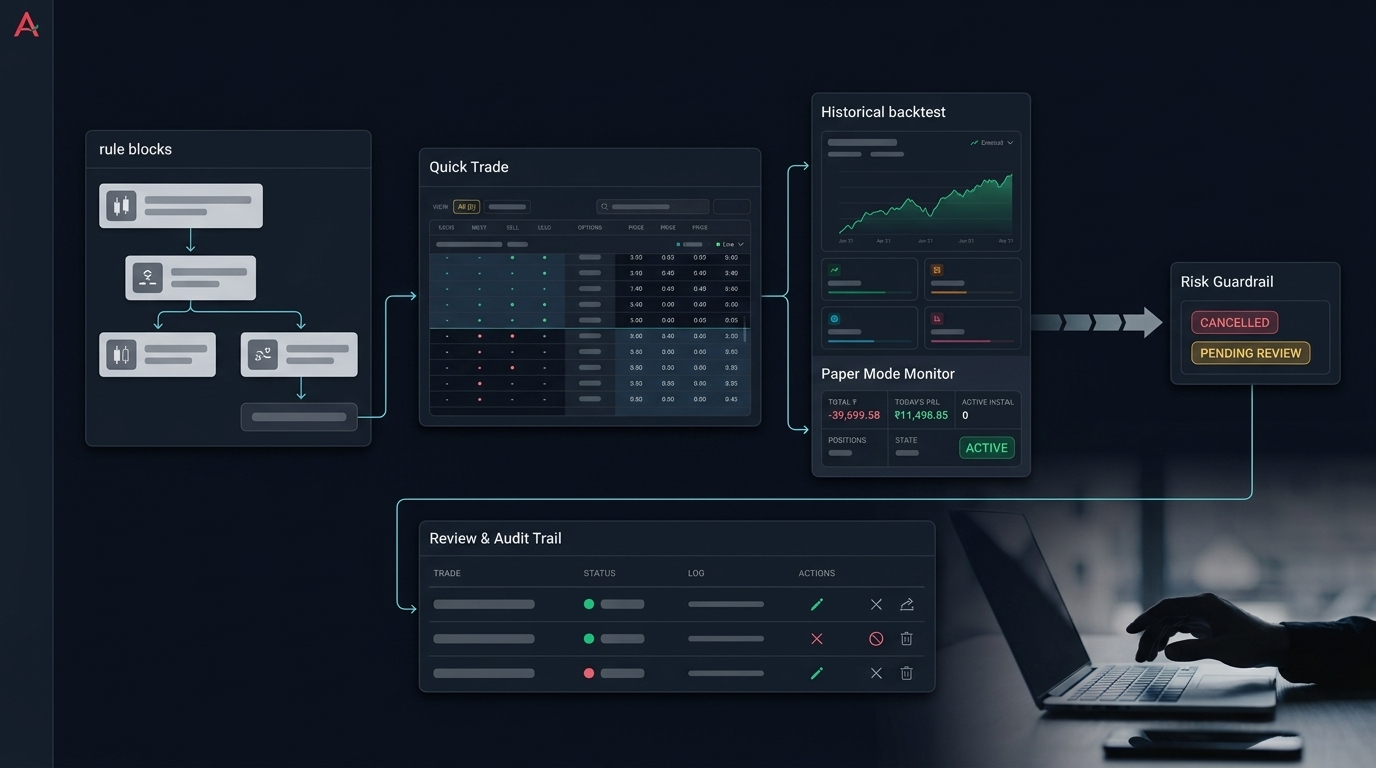

Step 2: Backtest on historical data

Once the rules are exact, you run them against past market data to see how they would have behaved. Backtesting answers a basic question: does this logic have any historical edge, or does it bleed money over time?

Look past the headline P&L. The numbers that tell you whether a system is survivable are:

- Maximum drawdown — the worst peak-to-trough fall in capital. Can you stomach it?

- Win rate paired with average win versus average loss. A system can win under 40% of trades and still be profitable if winners are larger than losers.

- Number of trades. Ten trades prove nothing; a few hundred across different conditions mean more.

Be ruthless about overfitting. If a strategy only works after you tune fifteen parameters to one year of Nifty data, it has memorised the past, not learned an edge. For options especially, your assumptions about fills, slippage, and expiry behaviour change the result a lot — the options backtesting workflow is worth understanding before you trust any equity-curve screenshot.

Step 3: Paper trade in live markets

A backtest uses clean historical data. Live markets are messier — spreads widen, orders get partial fills, data ticks arrive late. Paper trading runs your strategy on live prices with simulated money, so you catch this gap without risking capital.

Run it for long enough to see different market regimes: a trending day, a choppy range, and an event day like an RBI policy or expiry. If your paper results fall apart the moment volatility shows up, that is the system telling you something useful, for free. Paper trading is not an optional warm-up — it is the dress rehearsal that decides whether the strategy graduates.

Step 4: Broker execution, monitored

Only after paper trading earns its place does real money come in. Now your strategy connects to your broker and places live orders. The mechanics are usually a broker API connection — your platform sends the order, the broker routes it to the exchange.

Two things deserve respect here. First, start with small size, not your full intended capital. Live execution surfaces problems paper trading hides: session token expiry, rejected orders, margin shortfalls. Second, watch the order book, not just the P&L. Execution problems show up as failed or duplicate orders before they show up as losses, so an order audit view is part of your risk control, not an afterthought.

A simple worked example

Say your idea is an intraday Nifty momentum trade. The pipeline looks like this:

- Rule: Enter long if Nifty trades 0.15% above the first 30-minute high; stop at the 30-minute low; exit at 3:15 PM or on stop; risk capped at 1% of capital per trade.

- Backtest: Run two years of data. You find a 1.4 reward-to-risk ratio, a 38% win rate, and a 12% maximum drawdown. Survivable, not spectacular.

- Paper: Run four weeks live. You notice slippage on volatile opens eats more than the backtest assumed, so you widen the entry buffer.

- Live: Deploy with one lot. Monitor fills and order status daily before scaling.

Notice the strategy changed between steps 2 and 3. That is the workflow working — each stage taught you something the previous one could not.

Where retail traders go wrong

The failures are predictable, and almost all of them come from skipping the funnel:

- Jumping straight to live after a good backtest, with no paper stage.

- Confusing a scanner signal with a strategy. A scanner finds candidates; it does not define your entry, stop, or size. The signal is the start of the work, not the end.

- Ignoring risk limits. Per-trade risk, daily loss caps, and maximum open positions are not optional decorations. Set them before you deploy, not after a bad day. Sound risk management is the difference between a drawdown and a blown account.

- Set-and-forget thinking. Automation handles execution; it does not remove your responsibility to supervise. Broker sessions expire, data feeds hiccup, and news breaks your assumptions.

The takeaway checklist

Before any rule-based strategy touches real money, you should be able to tick every box:

- The rule is written in one exact, unambiguous sentence.

- It has been backtested across several hundred trades and multiple market conditions.

- You know its maximum drawdown and have accepted it in advance.

- It survived weeks of paper trading on live data, including a volatile event day.

- Per-trade risk, daily loss cap, and position limits are configured.

- You start live with the smallest possible size and watch the order book daily.

Algo trading does not remove risk or guarantee anything — it removes hesitation and gives you a system you can measure. The edge is in the discipline of the workflow, not in any single magic strategy.

If you want to walk this rules-to-live path on Indian markets with the tooling built in, you can request early access and start at the paper-trading stage where it is safe to learn.