Intraday algo trading sounds simple from the outside. Define rules, hit deploy, let the system trade. In practice, most days break in the boring details — a missed data tick, a stale token, an order that fires but never confirms.

This is a working checklist you can run before the bell and during the session. It is not a strategy recipe. It assumes you already have rules you trust and want to keep them from breaking on a live Indian market day.

The night-before checks

You do not want to think about plumbing at 9:14 AM. Handle the slow stuff the evening before.

Strategy state is clean. Confirm every active strategy is on the version you intend to run. If you edited entry conditions on Sunday, make sure the deployed copy reflects it. A surprising number of "the algo went rogue" stories are just an older version still running.

Holiday and expiry calendar. Check tomorrow's exchange status. NSE publishes holidays, special sessions, and expiry shifts. If it is a weekly expiry, your option strategies will behave very differently in the last hour — confirm your time-of-day filters are right.

Corporate actions on your universe. Splits, bonuses, dividends, and F&O ban list changes happen overnight. A stock entering the ban list means no new positions, only exits. If your scanner does not filter ban-list names, it will keep flagging them.

Capital and margin. Look at available margin in your broker terminal, not your spreadsheet. SPAN and exposure margins shift with volatility — what worked yesterday may need 8–12% more margin tomorrow if VIX moved.

Pre-market window (8:30 – 9:14 AM)

This is your real preparation window. Treat it like a pilot's pre-flight.

Broker login and token health. Most retail platforms force a daily login or TOTP refresh. Do it before 9:00. If you use a broker API directly, verify the access token has not expired and that order placement, position fetch, and funds endpoints all return 200.

Market data feed. Pull a last-tick check on the instruments you trade. If NIFTY shows yesterday's close at 9:10 AM with no update, your feed is stale. Cross-check against the exchange site or a second source.

Warmup candles loaded. If your strategy uses EMA200 on 5-minute candles, it needs roughly 525 prior candles. Confirm your engine has actually loaded that history — not just "started up cleanly". An indicator on partial data will fire wrong signals for the first hour.

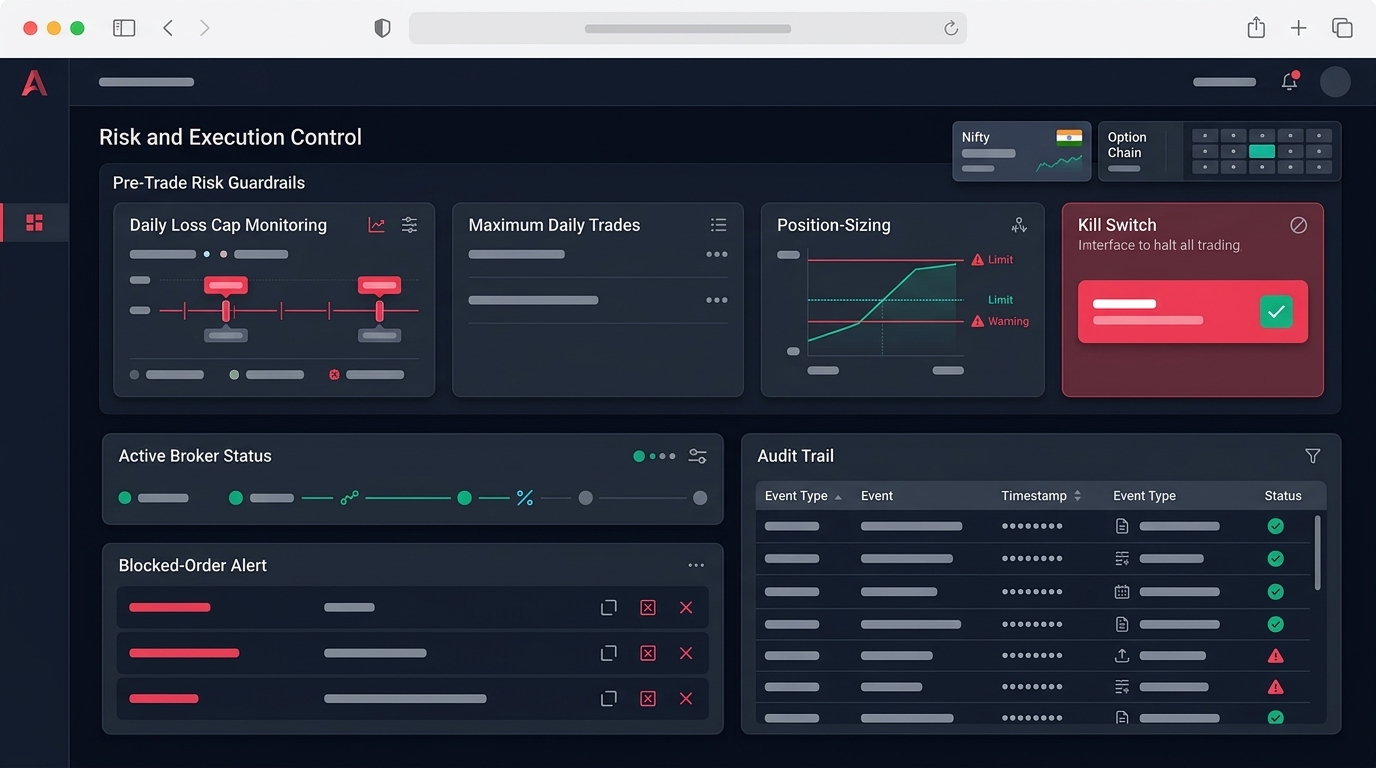

Risk caps set. Daily max loss, per-trade SL, max open positions, max lots per symbol. These should be configured per strategy, not at gut-feel level. A reasonable starting frame for retail is a daily loss cap of 1–2% of capital and per-trade risk under 0.5%.

Pre-market sentiment scan. Global cues, SGX Nifty (or GIFT Nifty), crude, and INR. You do not need to predict the day — you need to know if today is a normal-range day or a gap-and-go day, because your slippage assumptions change accordingly. Our weekly market outlook and a simple India VIX glance are enough.

The first 15 minutes

The 9:15 – 9:30 window is the noisiest part of the day. Many backtests look great because they silently include this window with mid-price fills. Live fills here are messy.

- Block new entries for the first 5–15 minutes unless your strategy is specifically built for the opening range.

- Watch the first fill latency. If your test order takes more than a second to confirm, something is congested — broker side, network, or feed.

- Reconcile positions. If your engine thinks you are flat but the broker shows a carry-forward F&O leg, stop and fix that mismatch before any new order fires.

Live-market checks (every 30 minutes or so)

Once the engine is running, you should not be staring at it. But you do want lightweight heartbeat checks.

Order-to-position reconciliation. For every filled order in the broker book, your engine should have a matching position. Mismatches are usually partial fills, rejections you did not see, or a freeze-quantity split.

Slippage tracking. Compare your model fill price to the actual average price. If a single trade slips 0.4% on a liquid name, that is a signal — not just a number to log. Wider-than-usual slippage often means thin liquidity or a fast move you should not chase.

Strategy P&L vs. cap. When realised + unrealised drawdown crosses about 60% of your daily loss cap, stop taking new entries. Let existing trades exit on their own SL. This is the boring rule that saves accounts.

Heartbeat from the engine. A working strategy builder or execution engine should emit a health signal every minute. No heartbeat for two minutes = treat as down, switch to manual oversight, do not assume it is fine.

Risk and execution rules that actually matter

A checklist without enforcement is decoration. The execution side is where retail intraday algos most often leak edge.

- Use limit orders with a small slippage band on liquid names. Pure market orders on illiquid F&O strikes are a common cause of bad fills.

- Cap the number of orders per minute per strategy. Runaway loops have happened to serious shops; you are not immune.

- Have a hard kill switch that flattens positions and disables new entries with one click. Test it on a Saturday with a paper account.

- Keep risk management parameters in config, not hardcoded inside the strategy. You want to tighten caps on volatile days without touching code.

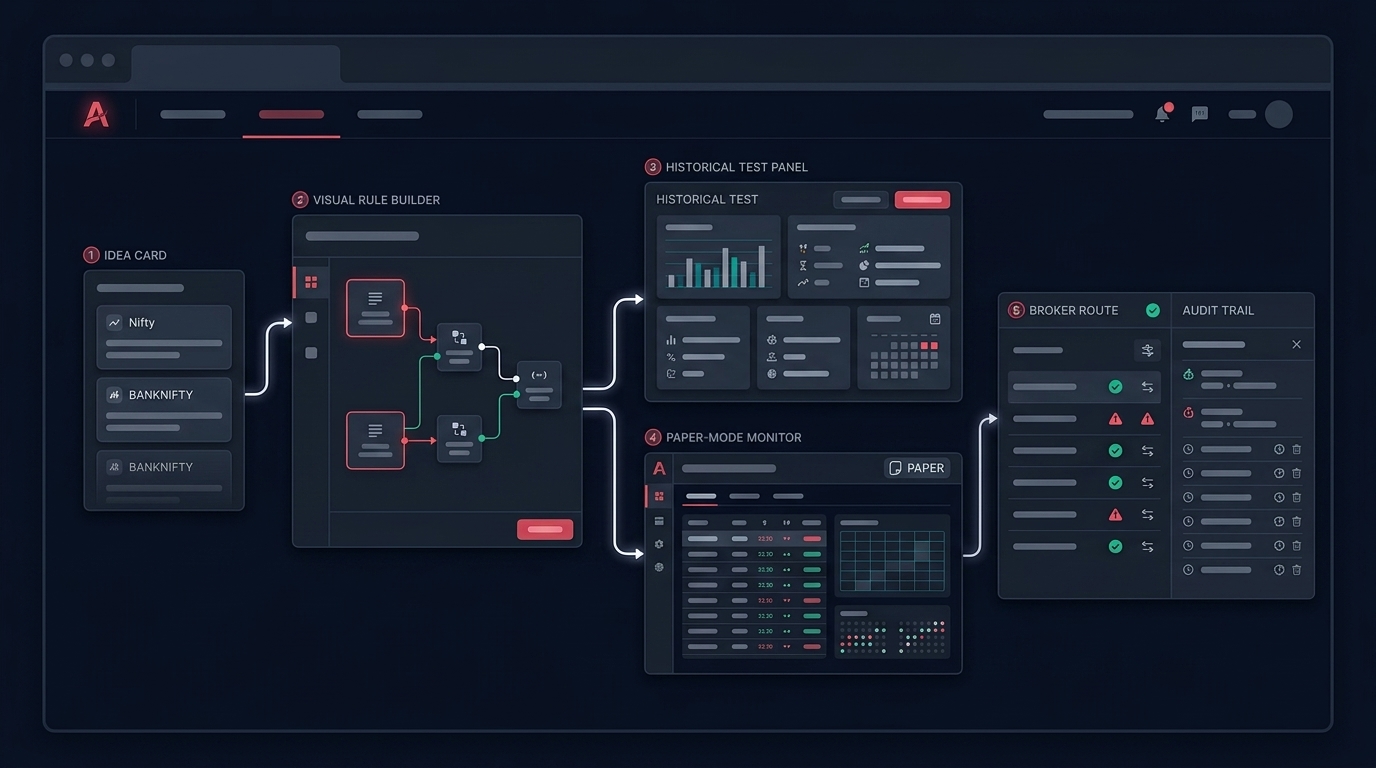

If you are still validating rules, run them through a backtesting cycle and then a forward paper run before any real capital. Indian options in particular need realistic slippage and freeze-quantity handling — assumptions that fail quietly in a backtest will fail loudly live.

The 3:20 PM and post-close routine

The day is not over at 3:30. The shutdown checklist matters as much as the open.

3:20 PM square-off pass. If your strategy is intraday-only, confirm every position has either exited or is queued to exit. MIS positions auto-square at the broker level, but they do it at market, often at the worst price of the day.

Order book sanity. Cancel any pending GTT or AMO that should not roll into tomorrow.

Trade journal. Export trades, slippage per trade, and which signals were ignored or rejected. Five minutes of journaling beats five hours of regret-driven re-coding on weekends.

Engine logs archived. Keep the day's strategy logs and order responses. When something looks wrong three weeks later, the log is the only honest witness.

A short checklist you can copy

- Night before: version, calendar, ban list, capital

- 8:30 – 9:14 AM: broker token, feed, warmup, risk caps, sentiment

- 9:15 – 9:30 AM: skip first-N-minutes, latency check, reconcile

- Through the day: order-position match, slippage, daily-loss gate, heartbeat

- 3:20 – 3:30 PM: square-off, pending orders, journal, logs

If you want a workflow that wires most of these checks in once instead of stitching them every morning, take a look at how we structure pre-market and live checks inside Anadi Algo — you can try it via early access.

Intraday algo trading is not won by faster signals. It is won by removing the small process failures that cost a percent here and a percent there. The checklist is the edge.