If you are searching for a QuantMan alternative, you have probably already run a few options backtests and hit the same wall most retail traders hit: a clean equity curve on screen does not automatically become a strategy you can run live with confidence.

QuantMan is a backtesting-first platform, and for a lot of traders it does that job well. The question is not "is it good." The question is whether a backtesting-first tool covers the whole workflow you actually need — from idea, to a realistic test, to a staged deployment, to live risk control. That full loop is where most comparisons should happen.

This post is a fair, workflow-level comparison. Use it to decide what you actually need, not just which logo looks nicer.

Start with what backtesting has to get right

Before comparing platforms, get clear on what a trustworthy options backtest requires. This is where most retail tests quietly lie to you.

Data and fill assumptions

For NIFTY and BANKNIFTY options, the result depends heavily on assumptions you may never see:

- Slippage and spreads. A short straddle that looks profitable at mid-price can flip negative once you assume realistic bid-ask fills, especially on far strikes or in the last hour.

- Expiry handling. Weekly expiry behaviour, settlement, and theta in the final two days dominate option-selling results. If the engine smooths over expiry-day mechanics, your backtest is optimistic.

- Liquidity at the strike. A backtest can "fill" a 200-point OTM strike that barely traded that day.

Whatever platform you pick, you should be able to inspect these assumptions, not just accept a number. We dug into this in detail in options backtesting for Indian traders — the same checks apply no matter which tool you use.

Overfitting and sample size

Twenty trades on one favourable quarter is not evidence. A believable options backtest needs enough expiries across different volatility regimes — a calm range, a trending move, and at least one VIX spike. If a platform makes it easy to tune parameters until the curve looks perfect, that is a feature working against you.

Where a backtesting-first workflow stops short

Here is the honest gap, and it is not specific to any one brand. Backtesting-first platforms are optimised to answer one question: did this idea work in the past? That is valuable. But traders need three more answers the test alone does not give:

- Is this strategy ready to deploy, or does it just look good on paper?

- What happens between a good backtest and a live order going to my broker?

- What stops it when live conditions stop matching the backtest?

When a tool is built mainly around the test, deployment and live guardrails often feel bolted on. You export a result, then improvise the live part — manual entries, a separate alert tool, a webhook somewhere, and no real staging step. That improvisation is exactly where retail money leaks.

What to look for in a QuantMan alternative

If you are switching, judge candidates on the full loop, not just the backtest screen.

Backtest realism you can audit

You want the same things listed above — visible slippage, expiry handling, and enough sample — but also the ability to re-run the test as rules evolve. A strategy is not one backtest; it is a version history. The honest version of this is walk-forward testing, where you validate on data the rules never saw.

A real path from backtest to deployment

This is the step most tools skip. After a backtest passes, there should be a staging stage — a place to review broker readiness, confirm the mode (paper or live), and save your risk assumptions before anything runs. Deployment should be a checklist, not a single "go live" button right after a green curve.

Live guardrails, not just alerts

A backtest cannot protect you at 2:30 PM on expiry. Live guardrails can: per-strategy stop, max loss for the day, position limits, and a manual override you can actually reach. If a platform's live layer is just "send signal to broker," you are missing the part that prevents one bad day from undoing a good month.

Paper-first before real capital

You should be able to run the deployed strategy in paper trading first, on live data, and watch order behaviour before committing money. Many backtest-first users discover only in live trading that fills, latency, or session expiry behave nothing like the test.

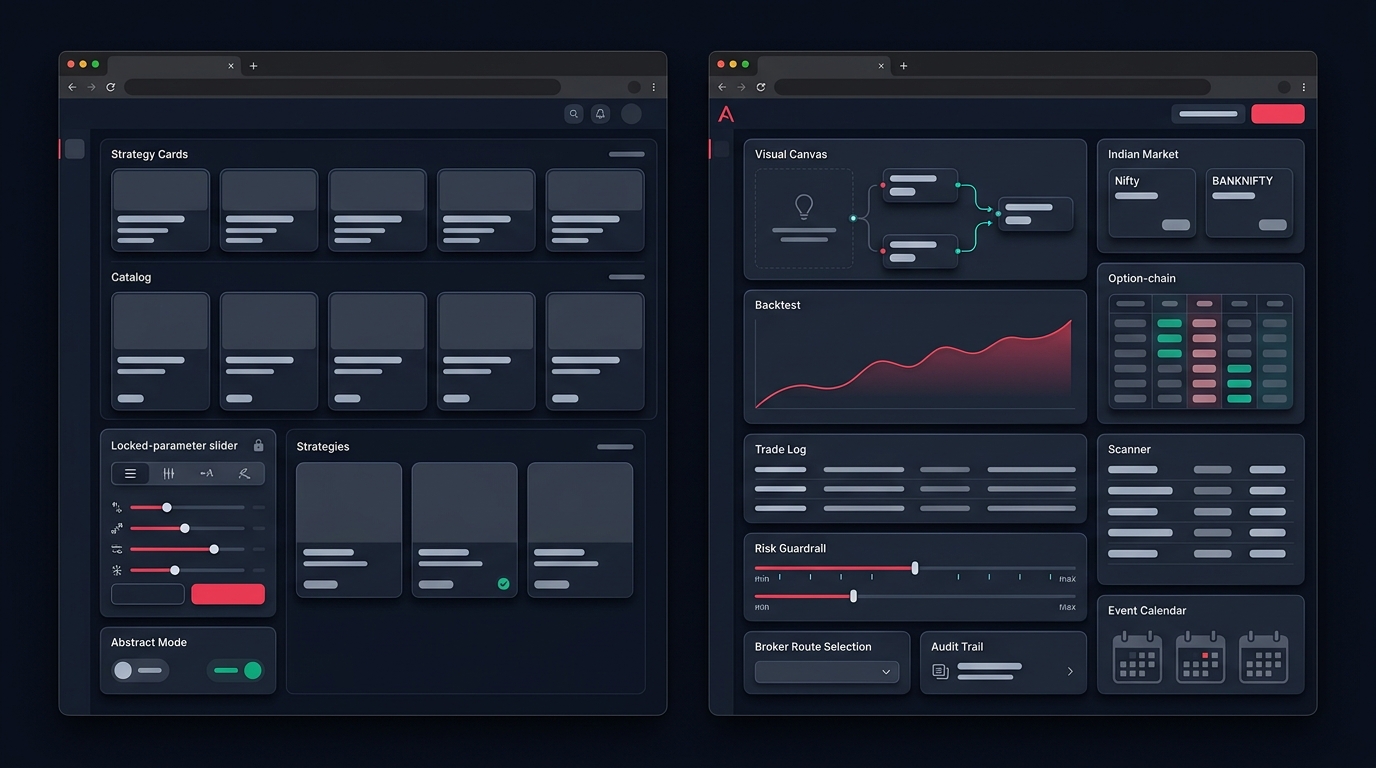

How Anadi Algo approaches the same workflow

Anadi Algo is built around the whole loop rather than the test alone, so the comparison is mostly about workflow fit.

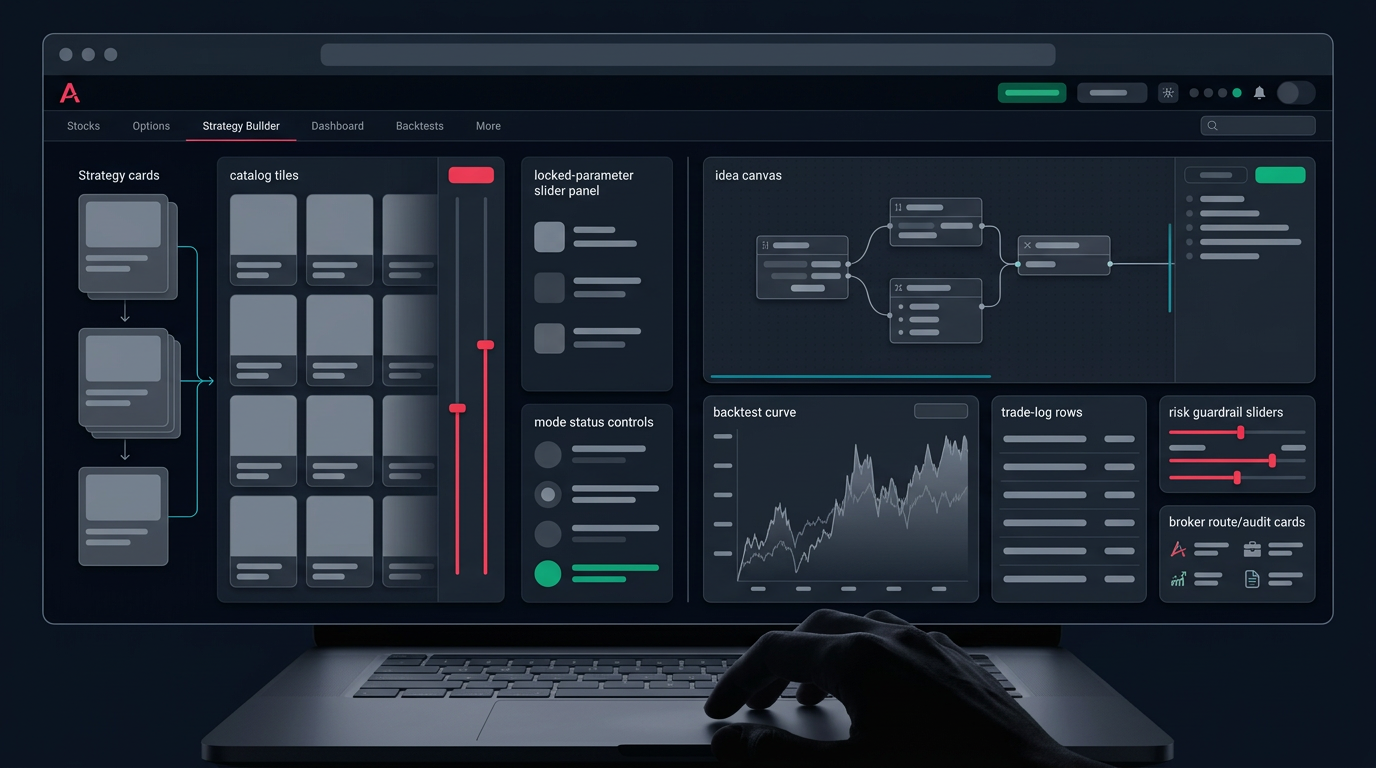

You build an idea in the no-code strategy builder, save it to a strategy library, and from that one place you can edit, backtest, inspect instances, or deploy. The library treats a strategy as something with a lifecycle, not a one-off export.

Deployment is deliberately a staging process. A Ready to Deploy stage shows broker readiness and the journey rule, asks you to review setup and save assumptions, and only then lets you start — separating "ready" instances from "running" ones, with the ability to move a running instance back for re-staging.

For options specifically, the workspace keeps chain inspection, OI, IV and theta, strategy finder, basket preview, and a margin estimate in one place, so risk and margin appear before execution rather than after. Time decay and volatility context sit next to the chain, not as an afterthought — which matters because correct direction can still lose money to theta drag.

And live trading is wrapped in risk management guardrails plus an order audit view, so broker execution is monitored, not a black box.

None of this makes the backtest itself less important. It just refuses to stop there.

A checklist before you switch

Use this on QuantMan, on Anadi Algo, or on any candidate. A real alternative should pass most of these:

- Can I see the slippage, spread, and expiry assumptions behind a backtest, and change them?

- Is my sample honest — multiple expiries across calm, trending, and high-VIX phases?

- Can I walk forward and re-test as rules change, instead of one frozen result?

- Is there a staging step between a good backtest and a live order, with broker readiness shown?

- Can I run it in paper mode on live data before risking capital?

- Are there live guardrails — daily max loss, per-strategy stop, manual override — not just signal forwarding?

- Can I audit orders by status and cancel where allowed, instead of assuming fills?

If a tool nails backtesting but fails the deployment and guardrail rows, you have found a good tester, not a complete workflow — and that gap is exactly what costs retail traders in live markets.

If you want to see the staged backtest-to-deploy flow on Indian options end to end, you can request early access and try the loop yourself before deciding what to keep.

The takeaway: pick your platform by the weakest part of your workflow, not the prettiest equity curve. For most options traders, the weak link is not the backtest — it is everything that happens after it.