A short strangle looks simple on a payoff diagram: sell an out-of-the-money call and an out-of-the-money put on the same expiry, collect premium from both, and profit if the underlying stays inside a range. Theta does the work. But the payoff diagram hides the part that ruins accounts — the two open tails on either side.

Backtesting is where you find out whether your range assumption survives real Nifty and BANKNIFTY behaviour, or whether a few gap and trend days quietly eat months of premium. This post walks through the three variables that decide a short strangle result: distance from ATM, volatility filters, and drawdown.

What a short strangle actually tests

You are betting on range, not direction. So the honest question a backtest must answer is not "how often did it win?" — a wide strangle wins most days by design. The real question is: when it lost, how badly, and could my capital have taken that hit without a margin call or a panic exit?

That reframing changes what you measure. Win rate is the least useful number here. Average loss size, worst single day, and the sequence of consecutive losses matter far more.

Distance from ATM: your first variable

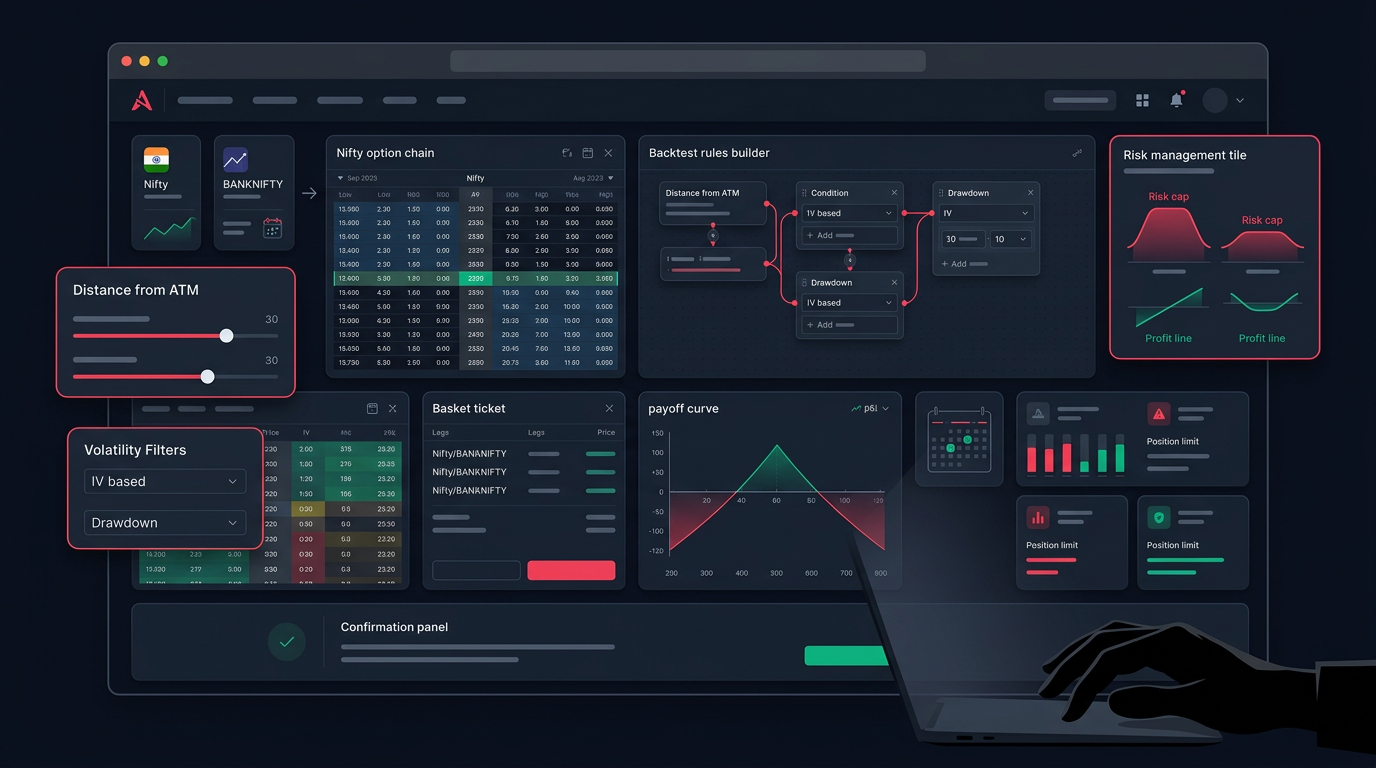

How far you sell the legs from the current spot is the single biggest lever in the whole strategy. There are three common ways to define it, and your backtest should pick one and stay consistent.

Fixed points vs delta vs standard deviation

- Fixed points from spot. Sell, say, 300 points OTM on each side of Nifty. Easy to code, but the meaning drifts — 300 points in a calm week is far, and in a volatile week it is nearly ATM.

- Delta-based. Sell each leg at a target delta, for example around 0.15–0.20. This keeps the "distance" consistent in probability terms as volatility changes, which is usually cleaner for a backtest.

- Standard-deviation based. Use the option-implied move to place strikes roughly one standard deviation out. This adapts to the current tape automatically.

The trade-off is the same across all three. Closer to ATM means more premium collected but a narrower range and more frequent tests. Wider means smaller premium, a higher raw win rate — and the same fat tail waiting on trend days. A wide strangle does not remove risk; it just moves the pain to fewer, larger events.

When you compare configurations, hold everything else fixed and vary only distance. If you change distance, expiry choice, and stop-loss all at once, you will never know which knob actually moved the result. This is where a structured options backtesting workflow helps — you want entries, exits, and costs defined once so each run is comparable.

Volatility filters before entry

Selling a strangle is selling volatility. So the question of when you sell matters as much as where.

Sell rich, not cheap

Premium is only worth collecting when it is priced generously relative to the actual movement that follows. Two filters retail sellers commonly test:

- India VIX / IV regime. Some systems only take short strangles when implied volatility is in a higher band, on the logic that you are being paid more for the same range risk. Others avoid entries when VIX is spiking hard, because that often coincides with the trend days that blow up naked premium. Both views are testable — do not assume, measure.

- IV percentile or rank of the underlying. Instead of the absolute number, look at where current IV sits versus its own recent history. Selling in the top part of that range is a different bet than selling near the bottom.

The point of a filter is to skip trades, and skipping trades is uncomfortable in a backtest because it lowers total premium collected. But if the days you skip are disproportionately the days you would have taken your worst losses, the filter earns its place. Check that explicitly: tag every trade with the entry-day VIX regime and see whether your largest losses cluster in one band. Reviewing IV and theta context before the trade — the way Anadi surfaces it inside the options desk — is the habit this filter is trying to build.

Event days deserve their own handling. RBI policy, budget, major expiry, and result-heavy sessions can break a range assumption on their own. Many backtests improve simply by excluding known event days rather than pretending the model handles them.

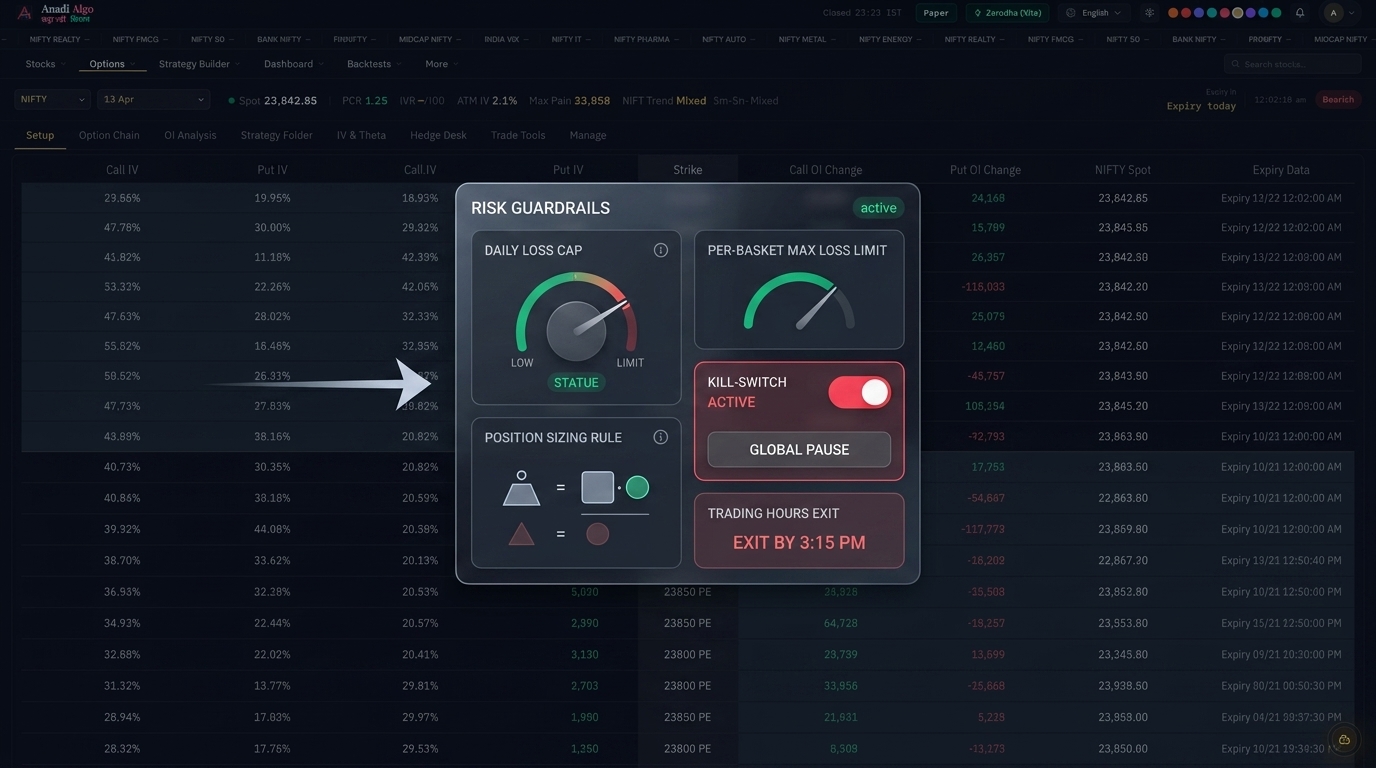

Drawdown is the number that matters

If you take one thing from this post: a short strangle backtest is judged by its drawdown, not its win rate.

What to actually record

For every backtest, log these:

- Max single-day loss. On a gap or trend day, one loss can equal ten to twenty days of collected premium. Know that ratio before you trade real size.

- Maximum drawdown. The peak-to-trough fall in your equity curve, in rupees and in percent of capital. This is the number that tells you whether the strategy is survivable at your account size.

- Consecutive losing days. Premium selling can win quietly for weeks, then string together losses when the market trends. Psychology breaks on the streak, not the average.

- Return relative to margin blocked. A naked strangle blocks real margin. A "good" P&L on a huge margin base may be a poor use of capital.

Model the exit, or the backtest lies

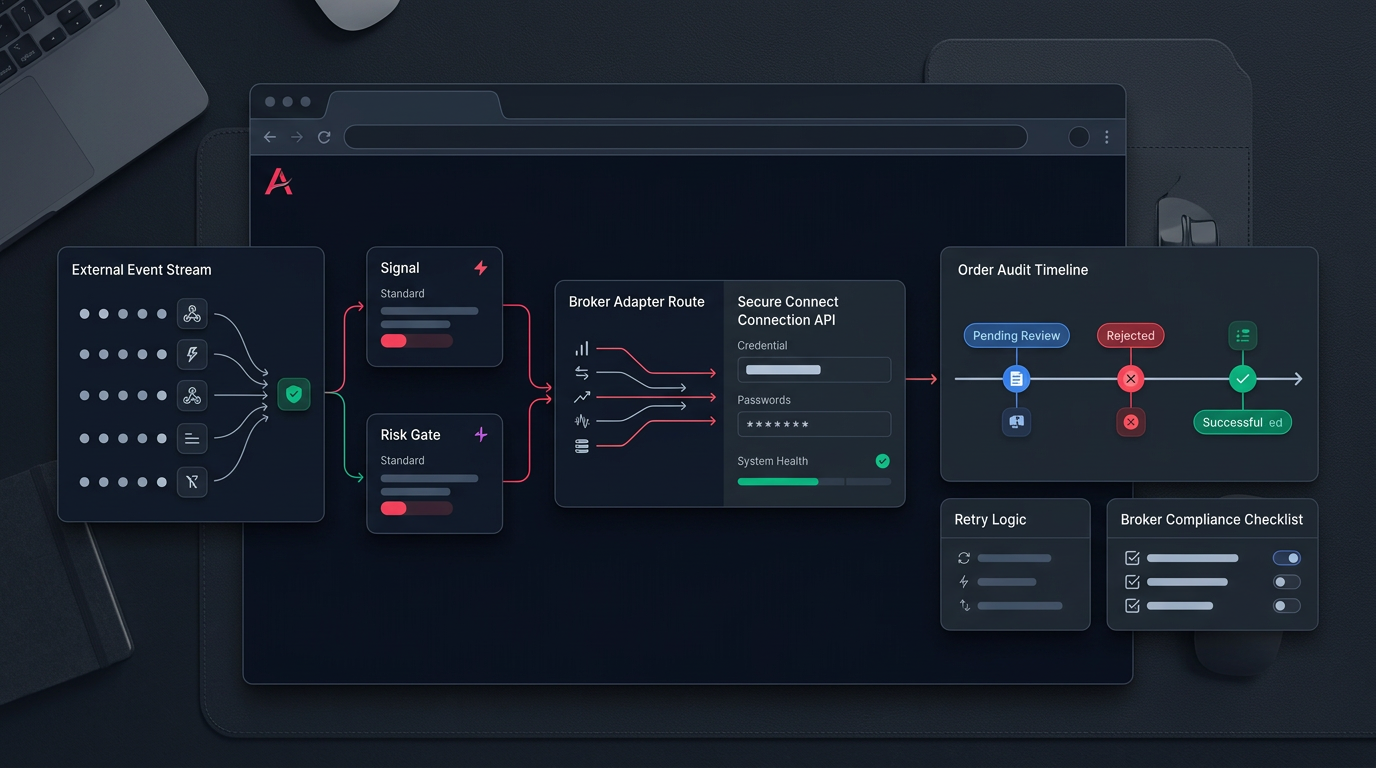

The most common way retail backtests overstate short strangle results is by assuming you hold both legs to expiry no matter what. In live trading you do not — you hit a stop, you adjust, or you get forced out by margin. If your backtest lets losers run to expiry but your live self would have cut at a 2x-premium loss, the two P&L curves are describing different strategies.

So define the exit in code: a per-leg or basket stop, a total-loss cap for the day, or a hedge that caps the tail. Testing a defined-risk version — buying further-OTM wings to convert the strangle into an iron condor — usually lowers the average return but makes the drawdown something you can actually live through. That is a trade many retail accounts should at least measure. Bringing protection into the plan up front, rather than as an emergency, is the whole idea behind treating hedging as part of the workflow.

Costs belong in the model too. Two legs in and two legs out means brokerage, STT, and slippage on four fills. On BANKNIFTY especially, slippage on wider spreads can quietly turn a marginal edge negative. Fold realistic costs in, and let your risk management rules — daily loss limit, max positions, sizing — be part of the test rather than an afterthought. If you are building the rules from scratch, a BANKNIFTY strategy builder lets you encode distance, filters, and exits as explicit conditions instead of vague intentions.

A short strangle backtest checklist

Before you trust a short strangle result, confirm you have:

- Fixed the distance rule — points, delta, or standard deviation — and varied only that when comparing.

- Defined a volatility filter and checked whether it removes your worst days, not just some trades.

- Excluded or specially handled event days (policy, budget, expiry).

- Recorded max single-day loss, max drawdown, and consecutive-loss streaks, not just win rate.

- Coded a real exit — stop, adjustment, or hedge — instead of holding blindly to expiry.

- Included four-leg costs and slippage, especially for BANKNIFTY.

- Compared naked vs defined-risk so you know exactly what protection costs you in return.

A short strangle can be a reasonable premium strategy, but only if your backtest respects the tails instead of averaging them away. Test the losing days as carefully as the winning ones, size to survive the worst run you saw, and let the drawdown — not the win rate — decide whether it goes live.

If you want to build and test these rules with clearer assumptions around entries, exits, and costs, you can get early access and run your own short strangle configurations before risking capital.