If you have used SpeedBot to build trading bots without writing code, you already know the appeal: describe your rules, backtest, paper test, then deploy. But at some point many traders start hunting for a SpeedBot alternative — usually not because the idea is wrong, but because their workflow has outgrown one piece of it.

This post is a fair, workflow-first comparison. No "we are better" noise. Just where SpeedBot fits, where a no-code trader tends to feel friction, and what to actually check before you switch.

What SpeedBot does well

Give credit where it is due. Based on SpeedBot's own site and third-party listings, it offers a genuinely broad no-code stack:

- A no-code bot creator with a large indicator library (SpeedBot advertises 200+ built-in indicators).

- Backtesting and forward/paper testing before going live.

- An options algo strategy builder plus a marketplace of ready-to-use public strategies.

- TradingView alert-to-trade routing, and automated stop loss, target, trailing SL, and daily limits.

- A mobile app and multi-asset bots (stocks, options, futures) from one dashboard.

That is a mature feature set. Pricing on directories like SoftwareSuggest is listed as "available on request," so treat cost as something to confirm directly rather than assume. If your need is "one platform, mobile-first, plug-and-play strategies," SpeedBot is a reasonable default.

Where no-code traders feel the gap

Most people looking for an alternative are not chasing more features. They are chasing a cleaner workflow. Three friction points come up again and again.

The scanner and the strategy live apart

A lot of no-code stacks let you build a bot on a fixed list of symbols. But real setups are discovered, not pre-listed. You want your bot to trade whatever is triggering a trendline breakout today, not a hardcoded watchlist you set last month.

When the scanner and the strategy are separate tools, you end up copy-pasting symbols and losing the exact signal that made the setup interesting in the first place.

"Breakout" gets flattened

This is subtle but expensive. Many builders reduce every pattern to "price crossed a high/low." A trendline breakout, a channel breakout, a flag, and a double-bottom breakout are not the same event, and a backtest that treats them identically will lie to you. If you cannot preserve the exact pattern name from scan to backtest to live, you are testing a different strategy than the one you saw on the chart.

Risk rules bolted on at the end

Stop loss, target, trailing SL, and daily loss limits should be part of the strategy definition, not an afterthought toggled at deploy time. If risk lives in a separate settings screen, it is easy to backtest without it and get a rosy equity curve that never survives a live drawdown.

What to check in any SpeedBot alternative

Before you move, run the platform through this checklist. It applies to any tool, not just Anadi Algo.

- Scanner-to-strategy continuity. Can a scan signal directly feed a strategy and a backtest, keeping the exact signal ID?

- Named patterns. Does it distinguish trendline breakout, channel, wedge, flag, triangle, and double top/bottom — or collapse them to highs and lows?

- Backtest realism. Can you set the fill model, fees in bps, capital per trade, and a dynamic (scanner-driven) universe rather than a static list?

- Risk inside the strategy. Are SL, TP, trailing stop, and daily loss limit part of the tested rules?

- Lifecycle. Is there a clear path from idea to saved strategy to backtest to deploy, with versions kept separate?

- Broker fit. Does it support your broker, and how does it handle session expiry and order rejections?

If a platform passes 1–4, your backtests will be far closer to live behaviour. That single thing matters more than indicator count.

How Anadi Algo approaches the same workflow

Anadi Algo is built around keeping scanner, backtest, and risk in one continuous path — the exact gap above. Here is the honest mapping.

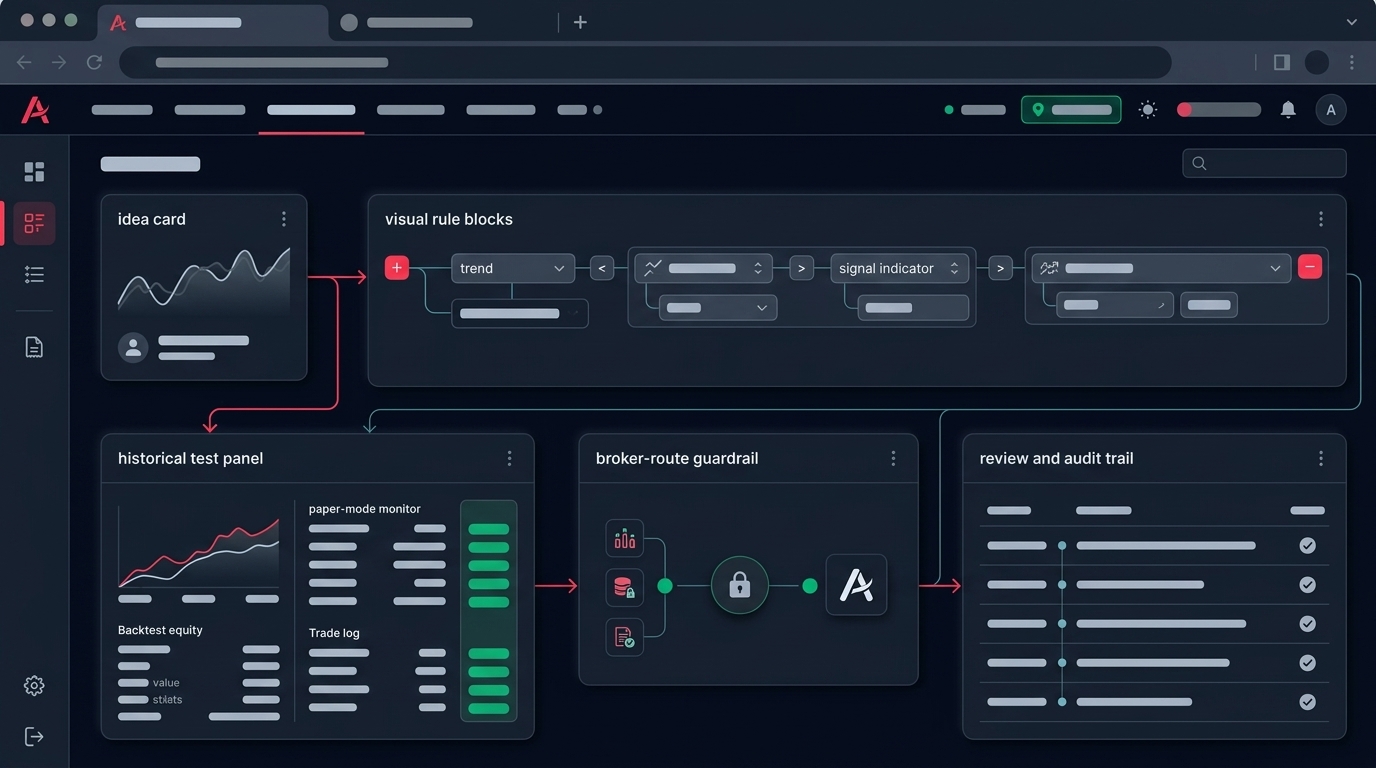

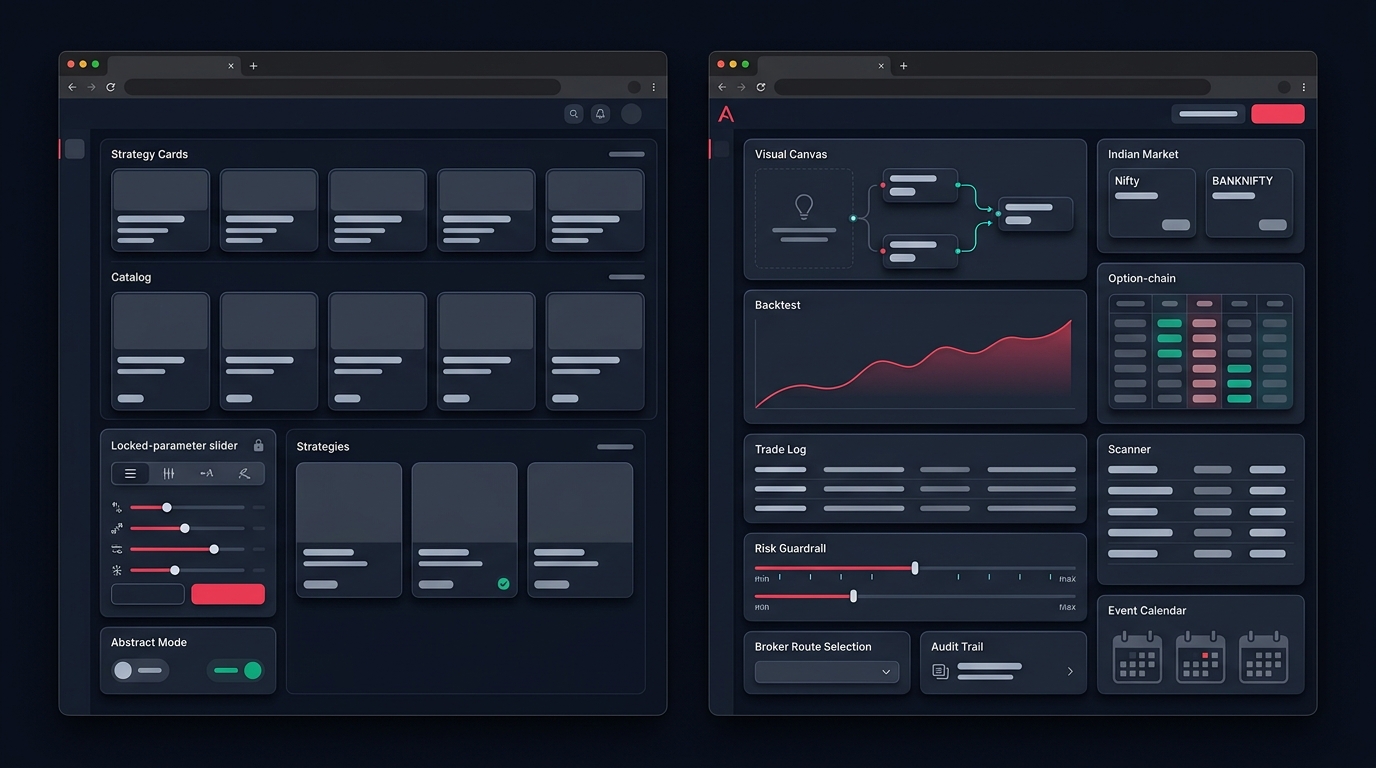

Ideas to rules without code

You start in plain language. The chat wizard asks for the missing pieces — entry, exit, risk, sizing, universe — and turns a Hindi or English idea into a structured strategy. From there the no-code strategy builder generates editable DSL, so you can see and adjust the exact rules instead of trusting a black box.

A scanner that keeps pattern names

The stock scanner shows ranked signal rows with the pattern label, score, timeframe, and freshness. Pattern IDs like trendline breakout, trendline breakdown, channels, wedges, flags, pennants, triangles, and double/triple tops and bottoms stay intact — and carry through to the strategy and the backtest. That is the "no flattening" point in practice.

Backtesting on the same universe you scan

In backtesting, you pick a static symbol set or a dynamic scanner universe, set the date window, fill model, fees in bps, capital per trade, SL/TP, and trailing stop, then launch. Because the backtest replays the same scanner signals your live setup uses, you are testing the strategy you actually intend to trade.

Risk as part of the rules

Stop loss, target, trailing stop, and daily limits are defined with the strategy, so your backtest and your live bot share the same guardrails. Pair that with a deliberate risk management layer and the equity curve you test is the one you deploy.

Quick workflow comparison

| Workflow need | SpeedBot | Anadi Algo |

|---|---|---|

| No-code building | Yes, bot creator + 200+ indicators | Yes, chat wizard + editable DSL |

| Named pattern scanner into strategy | Not the core framing | Core: exact scanner IDs preserved |

| Dynamic scanner universe in backtest | Not emphasised | Static or scanner-driven universe |

| Risk inside tested rules | SL/TP/trailing/daily limits available | Same, defined with the strategy |

| Ready-made marketplace | Yes | Focus is your own tested strategies |

| Availability | Live app, mobile | Early access |

This is not a scoreboard. If you want a marketplace of pre-built bots on mobile today, SpeedBot has the head start. If your priority is that what you scan is what you backtest is what you deploy, that continuity is where Anadi Algo is designed to win.

The honest takeaway

Switching platforms only pays off if it removes a real bottleneck. For most no-code traders leaving one tool for another, the bottleneck is the same: the scanner, the backtest, and the risk rules do not speak the same language, so live results drift from tested results.

Before you commit to any alternative, run this short check:

- Does a scan signal reach the backtest without losing its exact pattern name?

- Can you backtest on a dynamic scanner universe, with real fees and a fill model?

- Are your risk rules part of the tested strategy, not a deploy-time toggle?

- Is there a clean idea → save → backtest → deploy lifecycle?

- Does it support your broker and handle session expiry gracefully?

If you want to try a workflow built around that continuity, you can request early access and test your own scanner-backed strategy end to end. And if you are still surveying the field, it is worth a look at how different tools stack up when you compare algo platforms on workflow fit rather than feature lists.

The best alternative is not the one with the most indicators. It is the one where your tested edge and your live edge are the same thing.