The scanner fires. RSI crosses above 60. Price breaks out of a 20-day high. Volume is 2x the 10-day average. You see the signal and think: this looks solid. Let me automate it.

Most traders stop right there. That's the problem.

Going straight from scanner alert to live automation is one of the most common mistakes in retail algo trading. Not because the scanner is wrong — but because a scanner signal and a trading strategy are two different things.

What a Scanner Actually Tells You

A stock scanner filters instruments based on current market conditions. It says: "right now, this stock or contract meets these conditions." That's it.

It does not tell you:

- How often this condition has led to a profitable trade historically

- What the typical drawdown looks like after the signal fires

- Whether the setup works better in trending or range-bound markets

- How many of the hits are false breakouts

A scanner is a starting point. Treating it as the final step is where traders lose money.

The Missing Step: Backtest the Rules First

Before automating any scanner signal, run the exact same rules on historical data. Not a rough approximation — the same entry condition, the same filters, the same timeframe.

Backtesting forces you to answer questions your scanner never asks:

- Over the last 100 signals, what was the win rate?

- What was the average profit vs. average loss?

- How many times did the scanner fire and price reversed within two candles?

- What market conditions made the signal reliable vs. noisy?

If you skip this step, you're essentially testing live capital in real time.

Why This Step Gets Skipped

Honestly? Friction.

Translating scanner logic into backtest rules is harder than it looks. Scanners are built for quick visual filtering. Backtests are built for systematic rule testing. Different interfaces, different assumptions, often different data.

Add the excitement of a "working" scanner and the urge to start catching trades — and the validation step gets skipped every time.

How to Convert Scanner Rules into Backtest Conditions

Here is the practical workflow.

Step 1: Write the Signal Logic in Plain English

Before touching any tool, document your scanner rules as a precise trading rule set:

- Entry condition: What exact conditions must all be true at once?

- Exit condition: Fixed stop, trailing stop, time-based exit, or opposite signal?

- Filters: Trend direction, VIX range, time of day, sector?

- Universe: Nifty 500 only? Large-cap? Specific indices?

Example:

Enter long when RSI(14) crosses above 60, close is above the 20-day high, and volume is at least 1.5x the 10-day average. Exit at 2% stop loss or end of session. Apply only to Nifty 500 stocks trading above their 50 EMA.

If you cannot write this out clearly, the scanner logic is not ready to backtest — let alone automate.

Step 2: Match Your Scanner Logic to a Backtest Tool

The biggest translation error is using different parameters in your scanner and your backtest. If your scanner uses a 14-period RSI but you backtest with 9-period RSI, the results are meaningless. Same goes for timeframe, lookback windows, and volume calculation methods.

Use tools where the scanner and the backtest module share the same data feed and the same condition definitions. This removes the tool-mismatch problem before it becomes a live-trading problem.

Step 3: Look for Failure Modes, Not Just Win Rate

Don't stop at the headline number. Dig into:

- Signal frequency: Does it fire 3 times a week or 30? Both create very different risk profiles.

- Clustering: Do wins cluster in one market regime and losses in another?

- Drawdown windows: Was there a 3-month stretch where the signal consistently failed? Do you understand why?

- False breakout rate: How many signals led to an immediate reversal within the next two candles?

A signal with under 40% win rate can still be profitable if the risk-to-reward ratio is right. A signal with a 70% win rate can blow up if the losses are outsized. Both scenarios are invisible without the backtest.

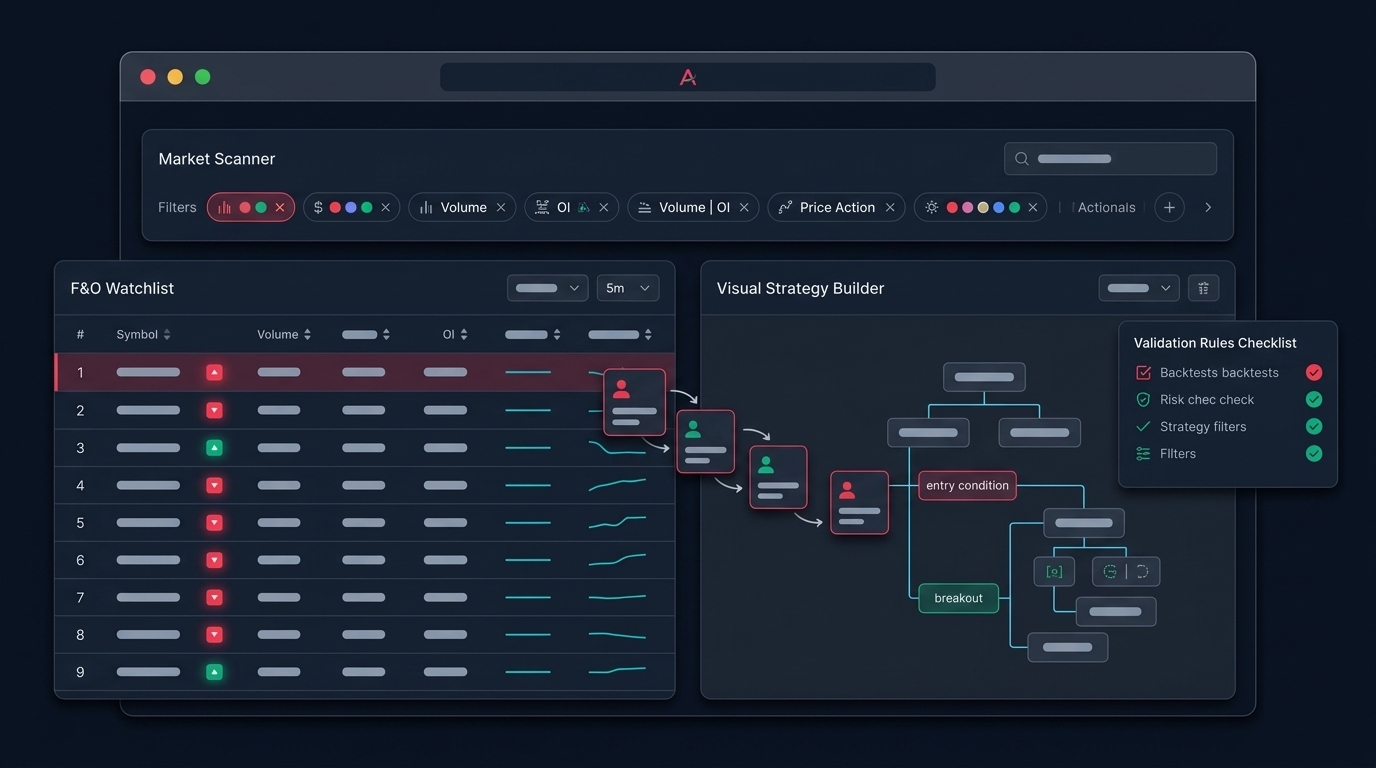

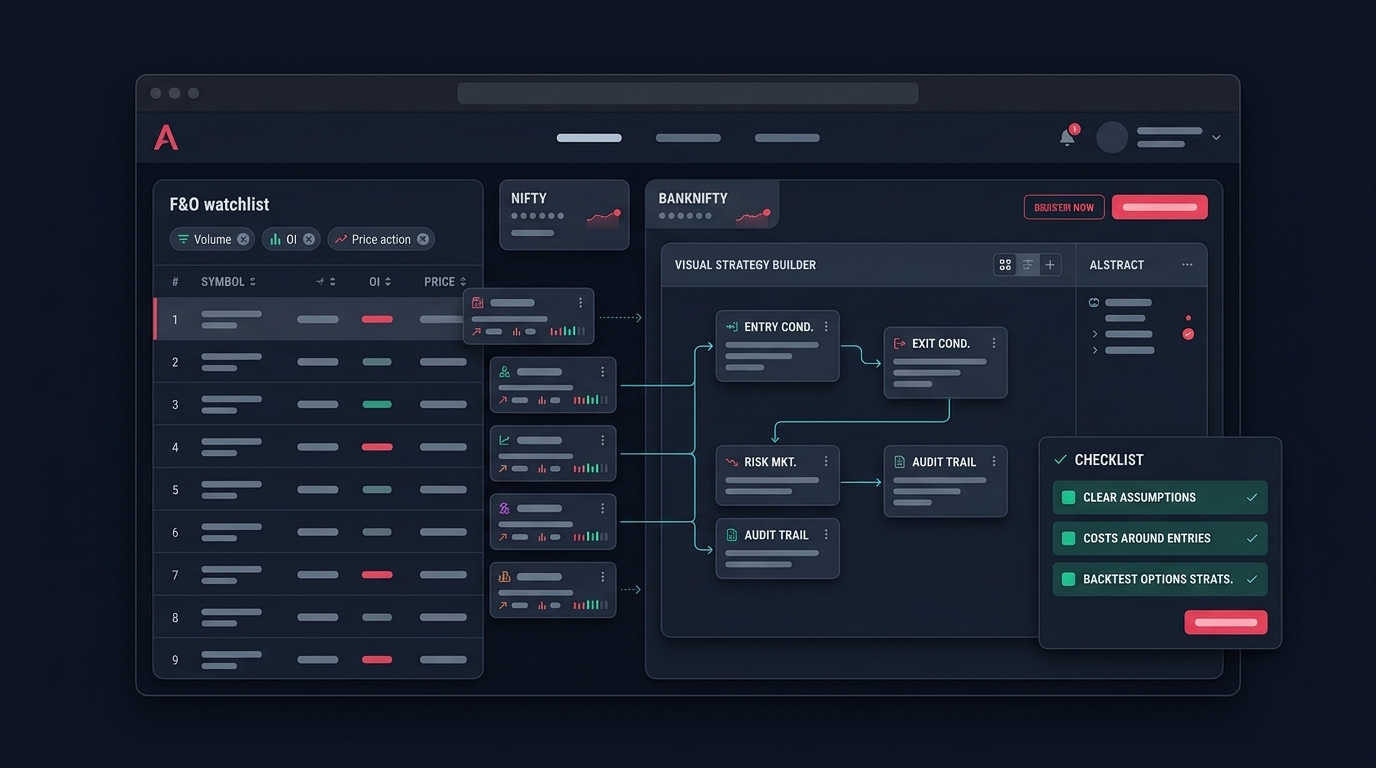

What to Check Before You Automate

Even after a solid backtest, run through this validation checklist:

1. Did the backtest use realistic cost assumptions? Slippage, brokerage, and market impact cost matter — especially in mid-cap or illiquid stocks. A backtest showing 0.5% average profit per trade may be unprofitable after real-world friction.

2. Does the scanner fire at the right time? Some setups fire on candle close. Others fire intrabar. If your automation triggers mid-candle on a condition designed for close-of-candle confirmation, your entry prices will drift. That drift compounds across dozens of trades.

3. Have you tested across market regimes? Run the backtest across at least one trending period and one choppy, range-bound period. A scanner tuned on 2023's bull run will behave differently in a volatile, sideways market.

4. Does it hold up on recent out-of-sample data? Split your historical data. If the signal works on 2021–2023 data but fails on 2024–2025 data, that is a warning sign — not a signal to automate.

5. Can you paper trade it first? Before committing capital, run the automation in paper trading mode for two to four weeks. Watch for execution issues, missed signals, and triggers that the backtest couldn't simulate.

The Right Order of Operations

Scanner setup → Backtest the exact same rules → Fix edge cases → Paper trade → Go live.

Each stage filters out one category of failure. Skipping any stage just moves those failures into live trading — where they cost real money.

If you are building scanner-to-strategy workflows and want to test your rules properly before automating, join early access to Anadi Algo where the scanner and backtesting module work on the same data layer with the same logic definitions.

Quick Validation Checklist

Before automating any scanner signal:

- Written the exact entry, exit, and filter conditions in plain language

- Backtested on at least 2 years of historical data

- Tested across both trending and sideways market regimes

- Reviewed signal frequency and false breakout rate

- Applied realistic slippage and transaction cost assumptions

- Confirmed scanner and backtest use identical parameter values

- Paper traded for at least 2 to 4 weeks before risking live capital

If even one item is missing, the signal is not ready to automate. That is not pessimism — it is how you stay in the game long enough for the good setups to actually pay off.