As of May 21, 2026, crude oil is once again the single variable that traders, analysts, and finance ministry officials are watching every morning. MCX crude has swung sharply through May, Brent has spent multiple sessions above $105 with brief pushes past $110, and the rupee has been printing fresh lows against the dollar. The trigger is geopolitical — Iran tensions, drone strikes on UAE and Saudi infrastructure, and uncertainty around the Strait of Hormuz — but the impact lands squarely on Indian equity portfolios, options books, and any system that wasn't designed for a high-volatility regime.

This post is not a forecast. It's a process post — what crude oil context means for the way you prepare, filter, size, and monitor your strategies in the current environment.

Why crude matters more than most Indian retail traders price in

India imports roughly 85% of its crude. That single statistic sits underneath almost every macro chain reaction you see in headlines.

When Brent moves from $80 to $110 and holds there:

- The import bill widens, current account deficit pressure rises, and the rupee weakens.

- Inflation expectations tick up, which complicates the RBI's room to cut rates.

- Input costs rise for paint, tyre, aviation, logistics, FMCG, and chemicals companies — margins compress unless they can pass costs through.

- Upstream oil companies see windfall potential, but downstream OMCs (BPCL, HPCL, IOC) get squeezed if retail fuel prices are kept stable for political reasons.

- FIIs trim exposure to net oil-importing economies, adding equity outflow pressure on top of the rupee weakness.

You don't need to predict any of this to trade. You just need to recognise that the correlation structure of the Indian market changes when crude is the dominant macro variable. Nifty IT and Nifty FMCG behave differently. Nifty Auto, Nifty Metal, and Nifty PSU Bank often lead the downside, as the March 13 and March 23 sessions earlier this year already showed — metal stocks dropped over 4% in a single session on Iran war escalation.

If your strategy was tuned on a low-VIX, range-bound 2025 dataset, this regime is a different statistical world.

What breaks first in algo systems during a crude shock

Three failure modes show up repeatedly.

Stoploss assumptions get violated by gap-downs

Crude shocks usually arrive overnight — a drone strike, a Trump statement, an OPEC+ surprise. Indian markets respond with gap opens, not orderly intraday slides. A system designed around an intraday stop on Nifty futures will see the stop skipped entirely. Backtests that assumed fills at the stop level overstate edge.

This is the standard gap risk problem, and it gets worse in geopolitically active months. If your backtest engine doesn't model gap behavior on overnight positions, your live drawdown will diverge from the equity curve you signed off on.

Option premia decouple from underlying movement

In a high-IV regime, option premia inflate on both sides. Selling premium feels lucrative until a single overnight headline expands IV further, vega losses hit the short leg, and margin requirements rise. Conversely, buying options at elevated IV often results in losses even when direction is correct, because IV crush after the headline resolves erodes premium faster than delta gain.

Both buyers and sellers face a different distribution of outcomes than the one their backtests probably saw.

Sector strategies built on stable correlations stop working

Pair trades between Nifty Bank and Nifty IT, or sector rotation models trained on 2023–2024 data, assume a certain correlation structure between sectors. In a crude-led decline, the correlation collapses or inverts. FMCG can hold green while metals drop 4%. Auto and PSU Bank can move together for reasons that have nothing to do with their usual driver.

If your strategy assumes stable correlations, it is now trading a market it doesn't recognise.

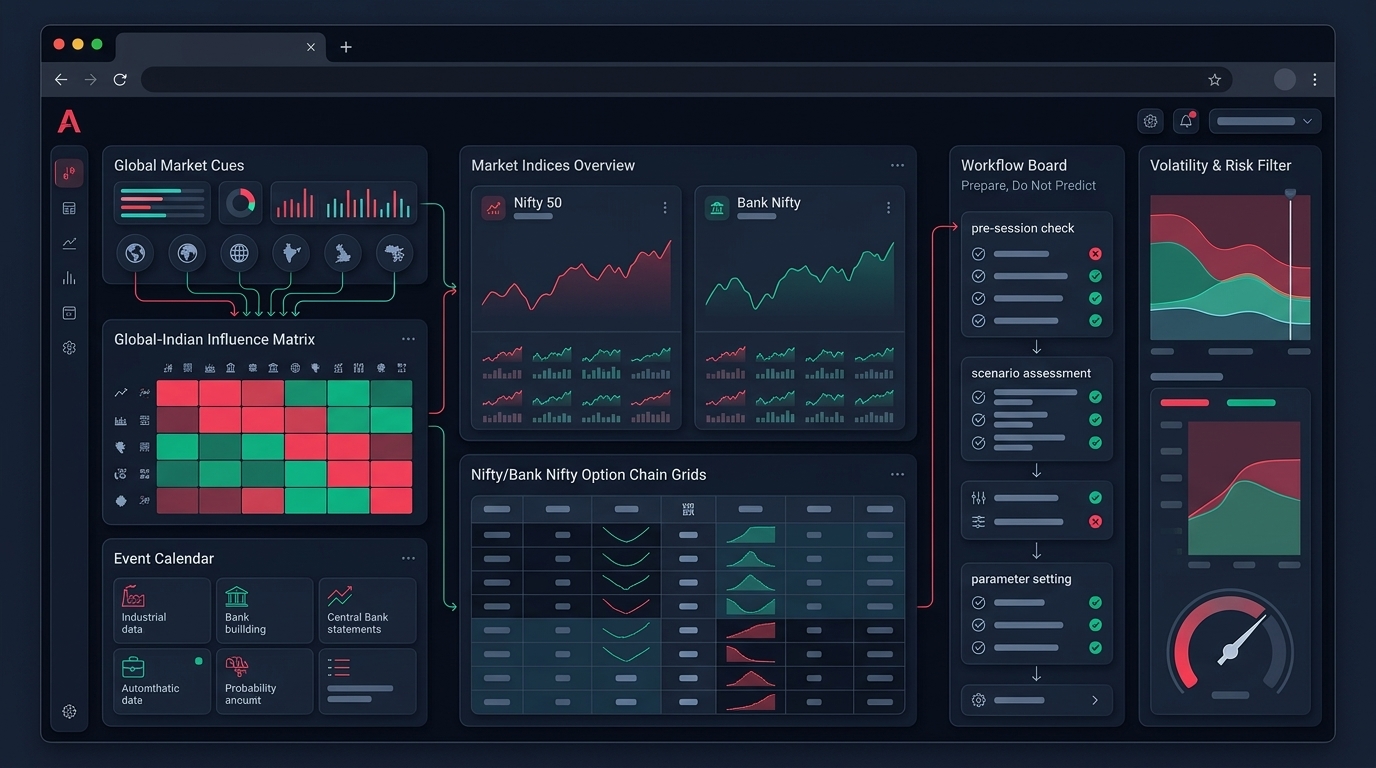

Risk filters worth adding right now

Adding filters is not about predicting the next leg. It's about giving your system a way to step aside when conditions don't match what it was built for.

A VIX regime gate

If India VIX is above your historical 80th percentile, run lower size or pause new entries. The exact threshold depends on your strategy — option sellers should be more aggressive about pausing, directional intraday systems can often handle elevated VIX with smaller size. The point is to have an explicit gate, not a feel-based decision.

If you trade options, the VIX regime filter discussion is worth revisiting before you size up this week.

A crude/rupee composite filter

Build a composite "macro stress" indicator using daily change in Brent (or MCX crude), USDINR, and India VIX. When all three are stretched on the same day, your system should know it's a stress day. The filter doesn't need to be sophisticated — a simple "two of three above threshold" rule already removes a lot of the days where retail strategies bleed.

A sector exposure check

Before market open, look at your strategy's effective sector exposure. If you're systematically long Nifty Auto and Nifty Metal — both crude-sensitive on the wrong side — you're stacking a single macro bet. Trim or rebalance. A good scanner workflow can surface this in seconds; doing it by hand in a hurry is where mistakes start.

Position sizing that respects gap risk

In a regime where overnight gaps are likely, intraday position sizing alone is not enough. Add an overnight haircut — most desks use 50–70% of the intraday limit for any position held overnight during high-VIX periods. The goal is to keep a single overnight surprise from erasing weeks of P&L.

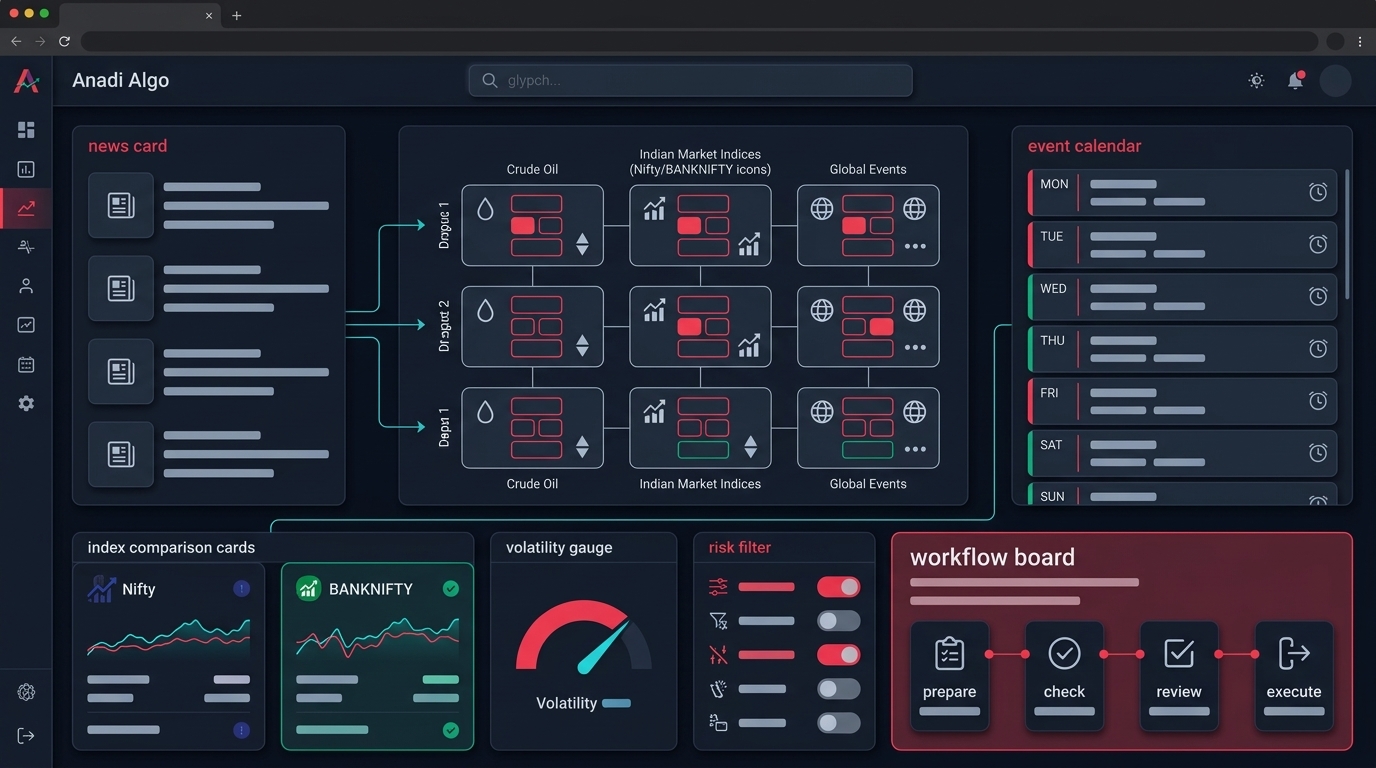

The event calendar matters more than ever

Headline-driven markets reward traders who respect the calendar.

Right now the key categories of event risk are:

- OPEC+ meetings and emergency calls — supply decisions can move crude 4–6% in a session.

- US-Iran diplomatic developments — peace talks, strike delays, or escalation can all move Brent by $5–10 within hours.

- Strait of Hormuz incidents — drone strikes, vessel seizures, or shipping disruptions trigger immediate risk-off responses.

- RBI policy commentary — given inflation pressure, even minor RBI signals on rate path can move bond yields and the rupee.

- Monthly inflation prints — CPI/WPI in a crude-elevated environment is no longer a routine data release.

- FII flow data — sustained outflow days compound rupee and equity weakness.

Build these into your strategy as no-trade or reduced-size windows. The earlier you set the window, the easier it is to enforce. A common pattern is to block new entries 60 minutes before and 30 minutes after a scheduled event, and to flatten or reduce overnight exposure ahead of unscheduled but high-probability windows (e.g., weekends during active conflict periods).

Backtesting in a regime you haven't seen before

Most retail strategies are backtested on the most recent 2–3 years of data, which means a lot of them were tuned during a relatively quiet 2023–2024 window. That introduces a specific blind spot.

A few things worth doing before you trust your equity curve in the current regime:

- Re-run on 2020 and 2022 data — the COVID shock and the Russia-Ukraine crude spike are the closest analogues. If your strategy survives those windows with acceptable drawdown, you have some evidence it can handle this one.

- Stress-test gap scenarios — synthetically inject 2–3% overnight gap-downs at random and check what happens to your stops, your margin, and your daily loss limits.

- Recalibrate slippage assumptions — bid-ask spreads on OTM options widen materially when IV is elevated. If your backtest used a flat slippage assumption, increase it.

- Check for survivorship in instrument selection — if you scan small caps or mid caps, your backtest universe might exclude names that got crushed and delisted. In a stress regime, those tail outcomes matter.

If you don't yet have a disciplined process for this, the options backtesting workflow is the place to start — get the data and assumptions right before you trust any equity curve.

Workflow checks before the market opens

A short, repeatable pre-market routine is more valuable than any forecast. The version that works for most algo desks in this regime:

- Crude check — MCX crude open, Brent overnight move, any weekend headlines.

- Currency check — USDINR opening level vs. previous close, DXY direction.

- SGX Nifty / GIFT Nifty — pre-market signal for likely Nifty open.

- India VIX prior close — and where futures suggest it might open.

- FII/DII data — previous day's cash and F&O activity.

- Active strategies inventory — what's running, what's the max loss for the day, what are the kill-switch levels.

- Event calendar for the day — economic data, F&O expiry proximity, scheduled corporate actions.

- Broker margin and order rejection logs — any pending issues from previous day that could affect today's execution.

This isn't glamorous. It's the difference between traders who blow up in a stress regime and those who don't.

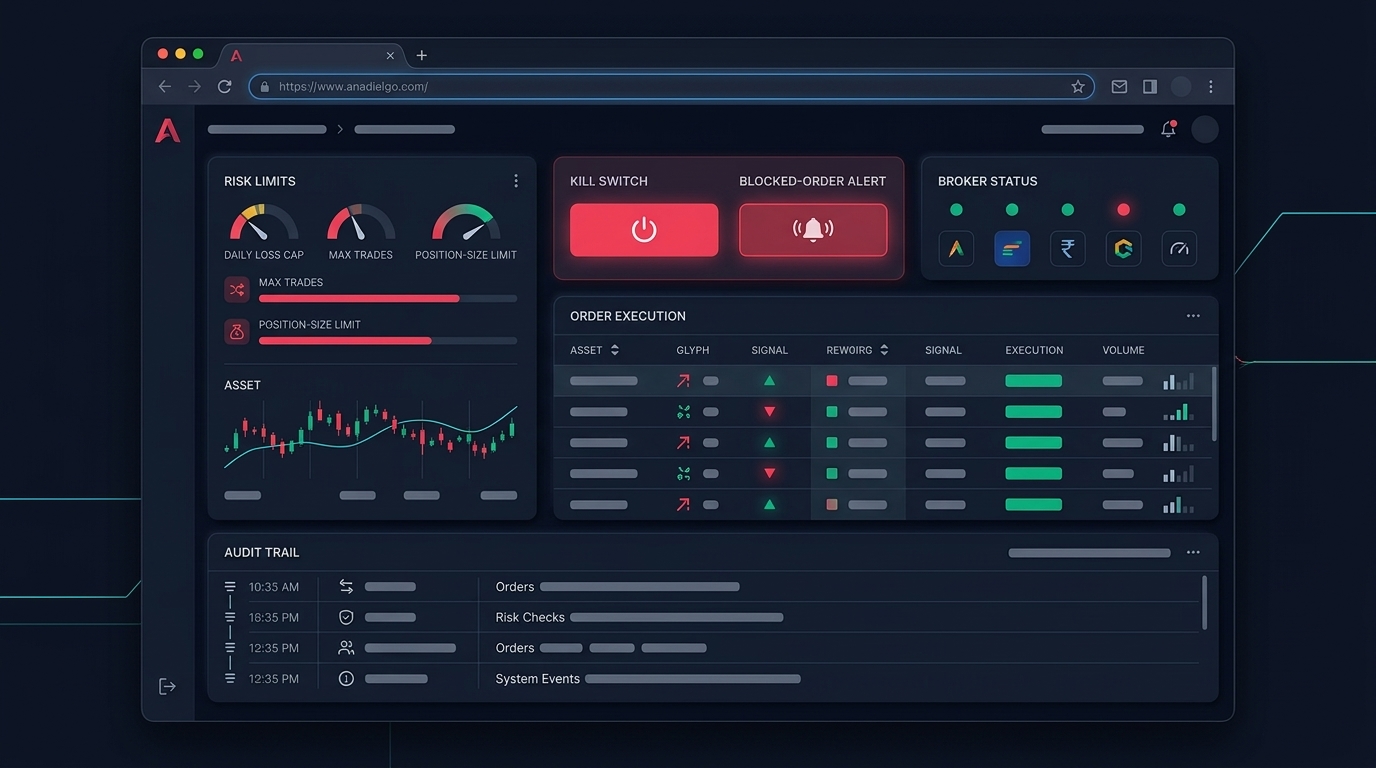

Where a structured platform helps

Most of the discipline above is process, not software. But process is easier to enforce when the platform makes the right thing the default.

A few specific places where this shows up in practice:

- A no-code strategy builder with explicit VIX, crude, and currency filters built into the entry logic, so the gate isn't something you remember — it's something the engine checks every cycle.

- A scanner that lets you watch sector exposure in real time, so you spot the crude-sensitive stacking before it becomes a problem.

- An execution layer with hard daily loss limits, kill switches, and per-strategy margin caps — so the worst day is bounded by code, not by willpower.

- Paper trading or staged deployment of any strategy that hasn't run in a high-VIX regime, before live size goes on.

If you want to see how this comes together end-to-end on Anadi Algo, you can request early access and walk through the workflow with a working strategy.

A practical checklist before the next session

- Is your strategy tested on at least one high-VIX historical window (2020 or 2022)?

- Do you have explicit gates for VIX, crude move, and USDINR move?

- Is your overnight position size capped below your intraday size?

- Are your stops modelled with gap behavior, not just intraday fills?

- Have you blocked entries around known event windows for the week?

- Is your kill switch on a daily loss limit live and tested?

- Do you have a 5-minute pre-market checklist that you actually run?

- Have you reviewed sector concentration in your active strategies today?

None of this predicts the next move in Nifty or crude. It doesn't have to. It just makes sure that when the regime turns hostile — and crude-driven regimes can turn fast — your system has the structural defences in place to keep you in the game.

The traders who survive these months aren't the ones who called the top. They're the ones whose process didn't change just because the headlines did.