A short straddle looks simple on a slide. Sell the at-the-money call, sell the at-the-money put, collect premium, wait for theta to do the work. In a backtest that ignores the messy parts, it can look like a money printer.

Live, it behaves differently. One trending day can erase a week of quiet premium. So before you commit real capital, the job is to define the rules tightly and test each one — not the idea in general, but the specific entry window, stop-loss, exit, and event filter you plan to actually use.

This post walks through the rules worth isolating in a backtest, with Nifty and Banknifty in mind. It is educational, not a strategy recommendation.

Why a vague short straddle backtest lies to you

The core problem with straddles is asymmetry. Your profit on any single day is capped at the premium collected. Your loss, if you sit through a directional move without protection, is not.

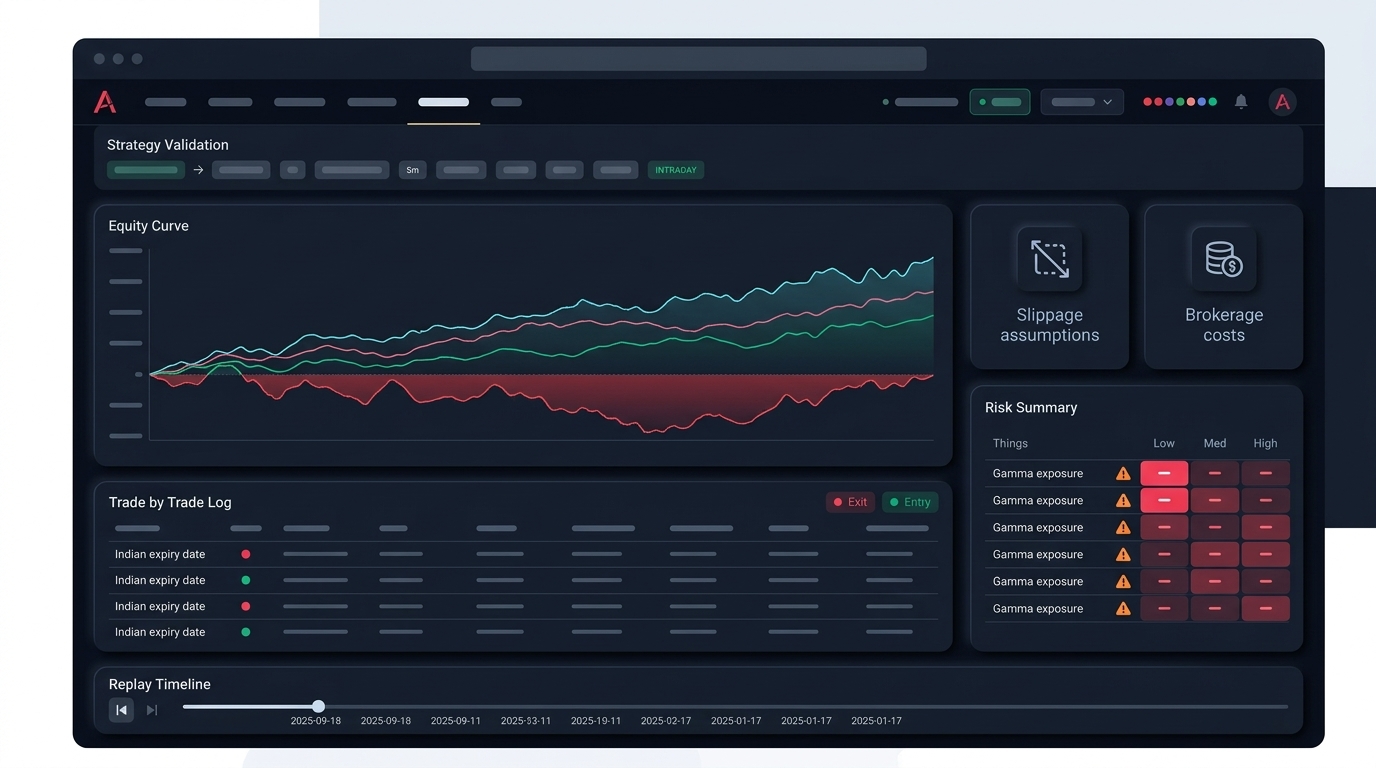

A backtest that runs "sell ATM straddle at open, square off at close" with no stops will average out a lot of good days against a few brutal ones. The equity curve might still slope up over a calm sample period. That curve hides the part that actually blows up accounts: the path. A strategy can be net positive over five years and still hand you a drawdown that forces you out before the recovery.

So the rules below exist to shape the path, not just the average. Each one is a variable you should test in isolation, then together — because they interact.

Entry window: when you arm the trade matters

The opening minutes of an Indian trading session carry the widest spreads and the jumpiest implied volatility. Premiums look fat, but slippage and a fast gamma move can punish an entry that is too early.

Things worth testing as separate entry rules:

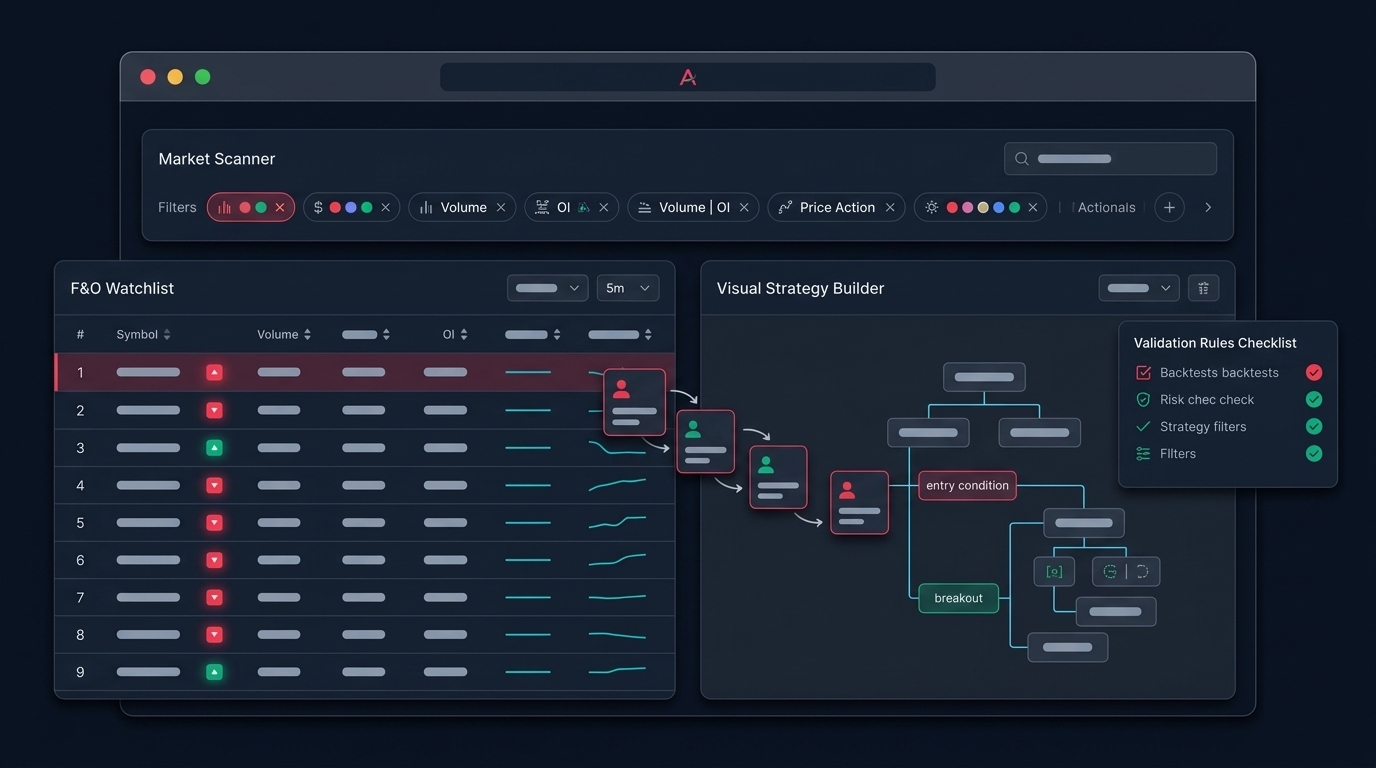

- Fixed time entry. Many option-selling frameworks wait until after the opening volatility settles — commonly somewhere in the 9:20 to 9:45 window — rather than entering at 9:15. Backtest a few fixed times and compare the distribution of outcomes, not just the mean.

- Strike selection at entry. "ATM" needs a definition. Is it the nearest strike to spot at entry time, or fixed at the previous close? On a gap day these differ a lot for Banknifty, where strikes are wider and moves are larger.

- Premium or IV threshold. Some rules only enter if total straddle premium or India VIX is above a floor, so you are not selling cheap volatility into a coiled market.

Banknifty moves more per point than Nifty, so the same rule produces very different risk. Test them as separate instruments. Do not assume a Nifty result transfers.

Stop-loss: the rule that decides if you survive

This is the rule that matters most, and the one most casual backtests get wrong. A short straddle with no stop is a bet that no large move happens — ever. That is not a strategy, it is a time bomb with good odds on most days.

Common stop structures worth testing:

Points-based stop on the underlying

Set a stop a fixed number of points above and below the entry strike — for example, a published Banknifty rolling-straddle approach used 200 points either side, with re-entry allowed only a limited number of times per day inside a defined window. The idea is to cut the position when the market starts trending instead of letting one leg run.

Backtest the trade-off directly: a tight points stop gets hit often on noise and bleeds via re-entries; a wide stop survives noise but takes bigger hits when it is finally wrong.

Premium-based stop per leg

Exit a leg when its premium rises to a multiple of the entry premium — say the leg doubles. This reacts to volatility, not just direction, which matters when both legs gain on an IV spike.

Combined / MTM stop

A stop on the total mark-to-market of the position, in rupees or as a percentage of margin. Simple to monitor live, but test how it behaves on gap opens, where the stop level is jumped over rather than touched.

Whatever structure you pick, model the re-entry rule explicitly. "Re-enter up to three times between 9:20 and 3:20" is a real rule with real costs. If your backtest re-enters infinitely, it is testing a strategy you cannot trade. For a deeper treatment of stop design, our guide on risk management covers position-level limits that sit on top of per-trade stops.

Exits: square-off time and profit locks

Exit rules are quieter than stops but they shape returns more than people expect.

Test these separately:

- Hard square-off time. Holding a short straddle into the close on a non-expiry day is different from holding it on expiry, where gamma is at its worst. Test a square-off well before close versus at close.

- Profit lock. Some rules exit once the position captures a set fraction of the entry premium — for instance, booking when roughly half the premium has decayed — rather than holding for the last rupee, which carries the most tail risk per rupee earned.

- Trailing the winner. Once in profit, trail a stop toward breakeven so a quiet morning does not turn into a red afternoon.

The point is to measure each exit's effect on the drawdown, not only the total return. An exit that shaves a little profit but cuts your worst day in half is usually worth it for a strategy whose entire risk lives in the tail.

Event filters: the days you should not be in the trade

Premium selling and known event risk do not mix well. The filter rules below decide which days you skip entirely — and skipping is a valid, testable decision.

- Expiry day. Gamma risk is highest near expiry, so a straddle held on expiry behaves nothing like one held three days out. Test expiry days as a separate bucket. Our post on gamma risk on expiry day explains why.

- Results and macro events. RBI policy, the Union Budget, major US data, and large index-constituent results can produce the exact directional gaps a straddle hates. Build a calendar filter and backtest "skip these days" versus trading them.

- Volatility regime. A VIX or premium-regime filter changes which days you even enter. Selling volatility when it is already crushed is a different trade from selling it when it is elevated.

When you test a filter, always compare the filtered result against the unfiltered one on the same sample. A filter that improves the average but only removes two trades is probably noise, not edge.

Cost and data assumptions that quietly decide the result

A short straddle is a high-frequency-of-trades, thin-edge strategy. That makes it unusually sensitive to assumptions most backtests gloss over:

- Slippage on entry and on every stop and re-entry. Stops tend to fill at worse prices precisely because the market is moving.

- Brokerage, STT, and exchange charges on four-plus legs per day add up fast against capped premium.

- Liquidity at your chosen strikes, especially far-month or deep strikes on Banknifty.

If your backtest assumes mid-price fills and zero costs, it is testing a strategy that does not exist. Run the same rules with conservative cost and slippage and watch how much of the edge survives. A realistic options backtesting setup that models entries, exits, costs, and slippage will give you a far more honest picture than a spreadsheet that fills everything perfectly.

A short straddle backtest checklist

Before you trade any straddle rule, confirm you have tested:

- Entry window and a precise definition of the ATM strike, per instrument

- A specific stop structure (points, premium, or MTM) with the exact re-entry rule modelled

- A square-off time and an optional profit-lock or trailing rule

- Event and expiry filters, compared against the unfiltered baseline

- Realistic slippage and full charges on every leg and re-entry

- Nifty and Banknifty tested separately, never assumed to behave the same

- The full drawdown path, not just the net return or win rate

Define each rule, test it on its own, then test the combination — and judge it by its worst stretch, not its best.

If you want to run these checks with cleaner assumptions, you can request early access and put your straddle rules through a backtest that takes costs and stops seriously before any live capital is on the line.